What You Need To Know Before Expanding To Southeast Asia as a Payments Company

What You Need To Know Before Expanding To Southeast Asia as a Payments Company

Breaking Down the Opportunities and Challenges for Payments Companies

This edition of our newsletter will identify opportunities for Payments companies looking to expand into Southeast Asia.

Leveraging the OIL Framework for Evaluating Market Opportunities for Payments Companies, which I introduced last week, we will assess and prioritize potential markets.

I will share valuable insights into the rapid digitization, evolving dynamics, and regulatory initiatives shaping the region's payments ecosystem.

This will allow you to discover how understanding these payment cultures is pivotal for payments companies and essential for merchants seeking to thrive in this era of innovation.

Payments companies in Southeast Asia often need more understanding of diverse consumer behaviors, regulatory challenges, and competition intensification if they want to stand any chance of succeeding.

If you might not have considered Asia for your expansion, remember that Asian payments companies have been some of the fastest-growing companies expanding to Europe and the U.S.

Taking their ability to leverage data to learn about trends shaping consumer behavior, companies such as TikTok, Shein, Alibaba, Tencent, Grab, Rakuten, and WeChat dominate not only in their own markets but have already grabbed significant market share in the Western markets.

Or, as Parag Khanna wrote in his best-selling book:

The Future is Asian.

In this newsletter, we will address Southeast Asia’s

Market Landscape and Trends

Regulatory Environment and Infrastructure Development

Digital Wallet Ecosystems and User Behavior

Opportunities and Challenges for Payments Companies.

Let me explain…

Let’s Limit Our Scope First…

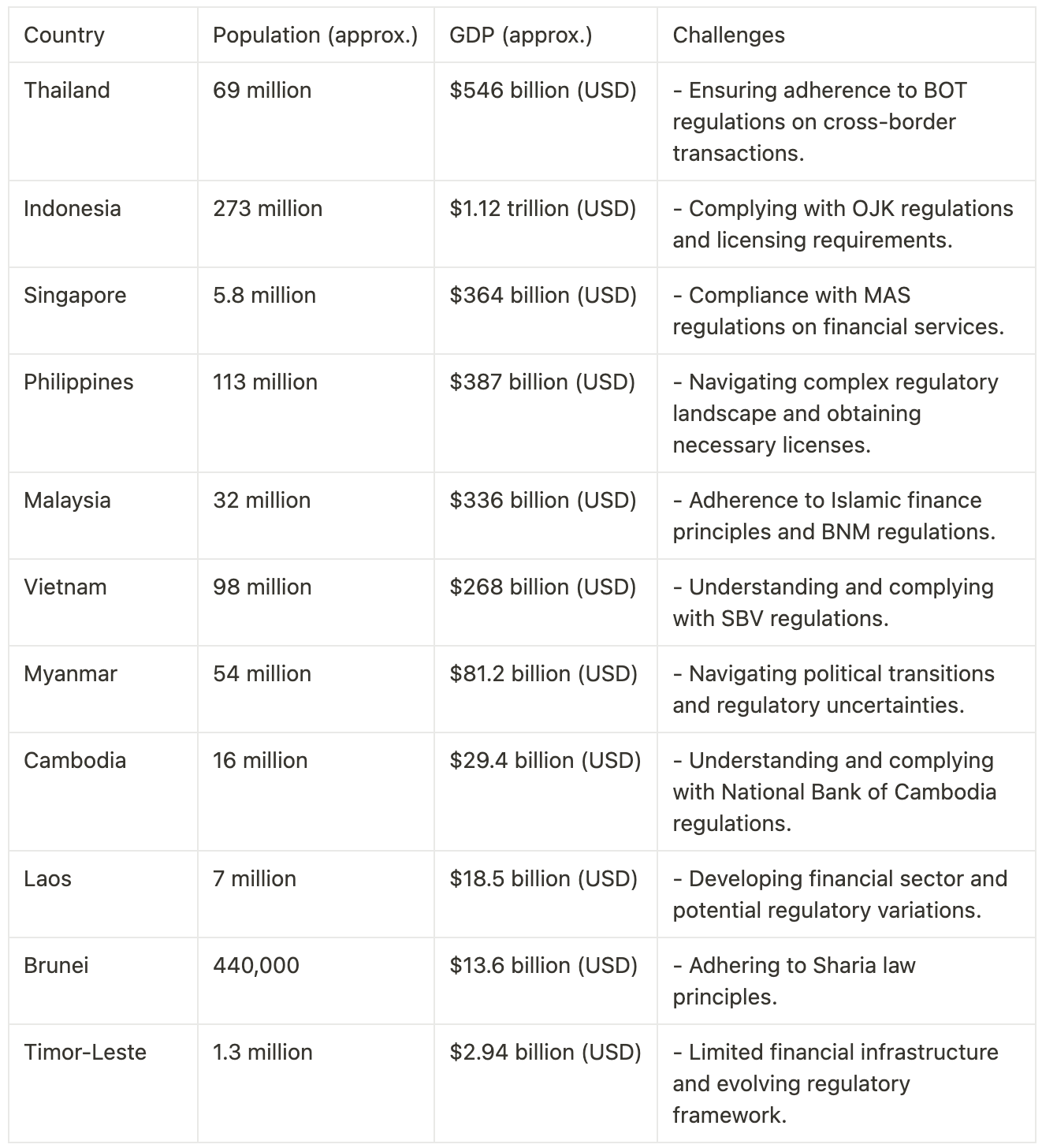

When discussing Southeast Asia, which consists of 11 countries, including Brunei, Burma (Myanmar), Cambodia, Timor-Leste, Indonesia, Laos, Malaysia, the Philippines, Singapore, Thailand, and Vietnam, I will limit my scope only to include Indonesia, Malaysia, Philippines, Singapore, Thailand, and Vietnam.

The criteria I used to do that include population, because their need to be enough consumers, who want to pay for goods and services, GDP to ensure their is enough of a sizeable market to go after, and any top-level challenges we would need to overcome.

Understanding the Market Landscape and Trends

Southeast Asia’s consumer payment landscape in contrast to the European or Northern-American’s, is currently experiencing a dynamic evolution mostly driven by rapid digitization, which reflect unique regional dynamics and preferences.

To understand the landscape, there are several key insights we need to review.

Because the Southeast Asia market has been booming in the last twenty to thirty years, most of the Payment methods that arose focused on serving local markets first.

Instead of card-based payments, the limitations of a formal banking system, the digitization and the high penetration of mobile phones were the perfect breeding ground for local alternative payment metheods that leverage QR-codes and stored-value digital wallets to arise.

The benefit in the immediate adoption of these digital wallets, was the ability to extract more data, especially around consumer behavior, that led to creating and embeddification of these wallets into super-apps such as GrabPay and ShopeePay.

The downside has been that many local payment methods have technically been consolidated with two or three major players who have captured significant market share and are top of mind for consumers whenever they pay.

A surprising development has been the rapid adoption of Buy-Now-Pay-Later payment methods, who leverage the same QR or stored-value digital wallets methods to pay, but essentially have provided a credit system, to mostly unbanked people, causing the further adoption of eCommerce to continue to grow.

As most of the Southeast Asia’s government are keen on becoming cashless nations, they have been supporting FinTech’s by providing easier regulatory frameworks, as well as stimulating micro-merchants as well as SME’s, to accept payments digitally, by making it easier to become a merchant, just using a cellphone.

In short, the 5 Trends that are shaping Southeast Asia’s landscape are;

The Rapid Evolution of Consumer Payment Methods

The Consolidation of Digital Wallets

The Acceptance of Buy-Now-Pay-Later

The Continued eCommerce Growth enabled by high Smartphone Penetration

Micro-Merchants Driving adoption endorsed by Government Incentives

Regulator Environment and Infrastructure Development

Compared to Europe and the United States, where regulatory bodies have focused on protecting consumers, while making it extremely difficult for Payments companies to innovate and develop new solutions.

In Southeast Asia, the majority of Governments understand that they need to collaborate with FinTechs, as they allow them to achieve their goals of transitioning into cashless societies.

Several Central Banks, including Indonesia and the Philippines, have been very open about their blueprint and roadmap to guide the digitization of local payment systems.

However, it even goes beyond just plans.

By collaborating with Fintechs, several projects have focused on developing Real-Time Payment Rails, ranging from P2P to leveraging QR technology.

Despite, having a European like mandate, these governments, also understood that for trade to continue to happen, they need to take Cross-Border payments in mind as well. This has led countries to establish bilateral cross-border connections between Indonesia, Malaysia, Singapore, and Thailand.

From a Payments Infrastructure Development point of view, this collaboration has created new initiatives like ASEAN’s Regional Payment Connectivity (RPC) and interoperable schemes like the Singapore Quick Response Code Scheme (SGQR+).

By continuing to build regional rails that can facilitate payments through the digital wallet infrastructure, Southeast Asian countries continue to forge their own path, without the relaince or restrictions global payments rails could have.

Digital Wallet Ecosystems and User Behavior

While the recent years has seen a significant drop in cash usage, for example Vietnam has gone down from 86% in 2017 to 42% by 2022, and even Singapore, has dropped from 40% to 19%.

Of course, a big driver in that has been the pandemic, however, the acceptance and rapid digitization of Southeast Asia’s countries, has been what has drove them into digital wallets, instead of to Card-based payments.

To understand that, we need to consider the following;

Locally alternative payment methods, have campaigned to help change consumer behavior, and preferences. This has allowed regional players to benefit from the adoption, leading to a consolidation mostly driven by rewards and highly targeted market campaigns.

With the digital wallet market now consisting of two to three major players, the ability for governments to introduce their initiatives has become much easier. Those fintechs' ability to operate in that country requires them to play by the rules the regulators created. The adoption is almost instant by building government-led initiatives and mandating that they are integrated into these apps.

On the otherside, the adoption is also stimulated to every one from local micro-merchants, to enterprise merchants. By removing any limitations on the micro-side, like minimum fees, there is almost no resistance to adopting the new payment methods. While on the enterprise side, digital wallets are promoted through cashback and discounts, or even connected to BNPL providers, which help boost conversion.

Opportunities and Challenges for Payments Companies

Now that we have an understanding of the market landscape, the trends, the impact of government on the infrastructure, and the adoption of digital wallets, we can identify the opportunities and challenges that exist for Payment companies looking to expand into the Southeast Asia market.

Opportunities for Payments Companies in Southeast Asia:

Untapped Market Potential: A significant portion of Southeast Asia's population remains unbanked, presenting a vast untapped market for payments companies to introduce inclusive financial services and solutions.

Evolving Consumer Preferences: The rapid shift towards digital payments, driven by changing consumer behaviors and increased smartphone penetration, provides opportunities for payments companies to innovate and capture market share.

Micro-Merchant Digitization: The ongoing digitization of micro-merchants offers opportunities for payments companies to facilitate cashless transactions, reduce fees, and provide value-added services, particularly in developing markets.

Cross-Border Payment Solutions: With the emergence of cross-border payment initiatives and regional connectivity, payments companies can create solutions that facilitate seamless and efficient cross-border transactions, catering to the region's diverse needs.

Integration with eCommerce: As eCommerce continues to grow, payments companies can collaborate with online marketplaces to offer convenient and secure payment options, leveraging the increasing trend of digital transactions in the region.

Innovative Financial Products: Payments companies can explore introducing innovative financial products, such as Buy-Now, Pay-Later (BNPL) options, to address credit access challenges and cater to the diverse financial needs of Southeast Asian consumers.

Challenges for Payments Companies in Southeast Asia:

Regulatory Complexity: Navigating diverse regulatory environments across Southeast Asian countries can be challenging for payments companies, requiring compliance with varying rules and standards.

Competition and Consolidation: Intense competition in the payments sector and market consolidation pose challenges for companies aiming to establish a strong foothold. Success often relies on effective differentiation and local adaptation.

Cash-Centric Habits: Despite digital advancements, cash remains deeply ingrained in certain consumer habits, especially in rural areas. Convincing users to transition to digital payments presents a significant challenge.

Security Concerns: The rise of digital transactions increases the risk of fraud and cybersecurity threats. Payments companies need robust security measures to gain and maintain consumer trust.

Infrastructure Disparities: Disparities in digital infrastructure, including internet accessibility and smartphone penetration, can limit the reach of payments solutions, particularly in less developed regions.

Consumer Loyalty Challenges: Southeast Asian consumers often switch between digital wallets based on promotions and discounts. Building and maintaining consumer loyalty can be challenging for payments companies.

Financial Inclusion Barriers: Despite opportunities in the unbanked market, overcoming barriers to financial inclusion, such as limited access to banking services and low financial literacy, requires concerted efforts.

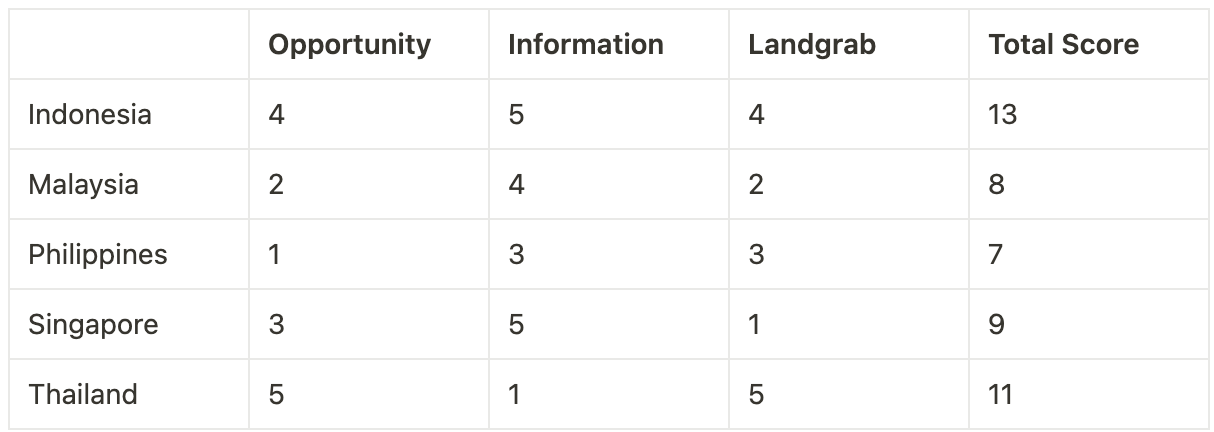

Turning research into an assessment using the OIL Framework

Now that we have done this research, have a good understanding of the landscape, how would we turn that into helping us decide to research further or where to expand to.

I would use the OIL Framework, which stands for Opportunity, Information, and Landgrab.

So for example, let’s say you are a European Payments company, who wants to expand into Southeast Asia, we would use research as the above but much broader and in-depth into each country to score each country as a potential expansion market.

While we have used the OIL Framework to assess the Southeast Asian market opportunities, I would consider this just the beginning of any proper assessment.

The Southeast Asian market has a lot of opportunities, but things might not be as easy as this assessment could lead you to believe.

That is why you need to DO YOUR OWN RESEARCH and dive deep to determine if it is right for your payments company.

Thank You for Reading. Feel free to Like, Comment, Share, or Post on Your Socials.

P.S. Whenever you're ready, this is how I can help you:

1-on-1 Video Call with Dwayne Gefferie: If you want to solve your Payments challenge quickly, get direct answers based on 20 years of experience and continuous market research, develop a Strategy, validate your idea, or discuss a product feature. Book a 1-on-1 Video with me. [Limited Available Slots].

If you want to work with me in a larger capacity, either speaking, advisory, or consulting, feel free to email or DM me.

Thanks for the insights Dwayne. Well articulated and handy. Will deep dive into your post on the OIL framework.

Being in the fintech space and payments company, SEA and MENA are geographies we are expanding into.

Looking forward to more insights!

Cheers,

RR