Usage-Based Billing

Why Adyen, Stripe, Airwallex and Salesforce are all buying the same software, and what they're really paying for.

Adyen doesn’t buy companies. For twenty years, that was the whole point.

Then it bought two in seven weeks.

In April, Adyen paid €750 million in cash for Talon.One, a Berlin loyalty platform, made its first acquisition in its history. Eight weeks later, on 11 June, it signed a second: $335 million for Orb, a usage-based billing startup out of San Francisco. The deal is set to close on 1 July.

Look at when this happened. The timing tells us a lot.

In February, Adyen reported its second-half 2025 numbers, and the stock dropped about 20% in a day. Net revenue grew 17%. The problem wasn’t the result.

It was the outlook. Adyen guided to 20%-22% growth for 2026, a shade under what analysts wanted, from a company the market had priced for more. Berenberg cut its target from €1,550 to €1,000 and still called the platform best-in-class.

That’s the bind Adyen is in. It can meet expectations and still watch the stock fall. It happened before, in August 2023, when a single soft quarter knocked 39% off the share price in a single day.

So picture a company whose growth is settling into the low twenties, trading well below its highs, under pressure to find margin somewhere new. In that window, it breaks its founding rule twice and rolls out an agentic-commerce suite at the same time. At a retail show this spring, it demoed a setup where autonomous agents shop on a merchant’s behalf.

For a firm that spent two decades insisting it would build whatever it needed, that’s a real change of posture. Every one of those moves points the same way: toward owning more of what happens around the payment, not just the payment itself.

This isn’t Adyen buying more processing. It’s Adyen buying a different layer.

And it’s not the only one.

One move, four buyers

In about six months, four of the best engineering shops in software and payments made the same move.

Stripe bought Metronome. Adyen bought Orb. Airwallex bought OpenPay, then Leapfin. And Salesforce, which isn’t a payments company at all, bought m3ter.

Different firms, different continents, one target: the software that meters what a customer uses, prices it, bills it, and books the revenue.

Usage-based billing.

Two editions ago, I put the whole M&A wave on a single grid. One column kept lighting up for the firms whose payment rails were already finished. They weren’t buying rails. They were buying the cart, the layer that decides on the payment before it happens.

This is that column, up close.

Here’s my read, and the rest is the argument for it. A processing fee gets cheaper as it scales, because any rival can undercut it by a few basis points. A billing system gets harder to leave as it scales because it is wired into how a company sets prices, books revenue, and closes the quarter.

The rail commoditizes. The meter compounds. And AI is accelerating the meter compound.

What the layer actually is

Quick definition, because “billing” is one of those words everyone nods at and nobody pins down.

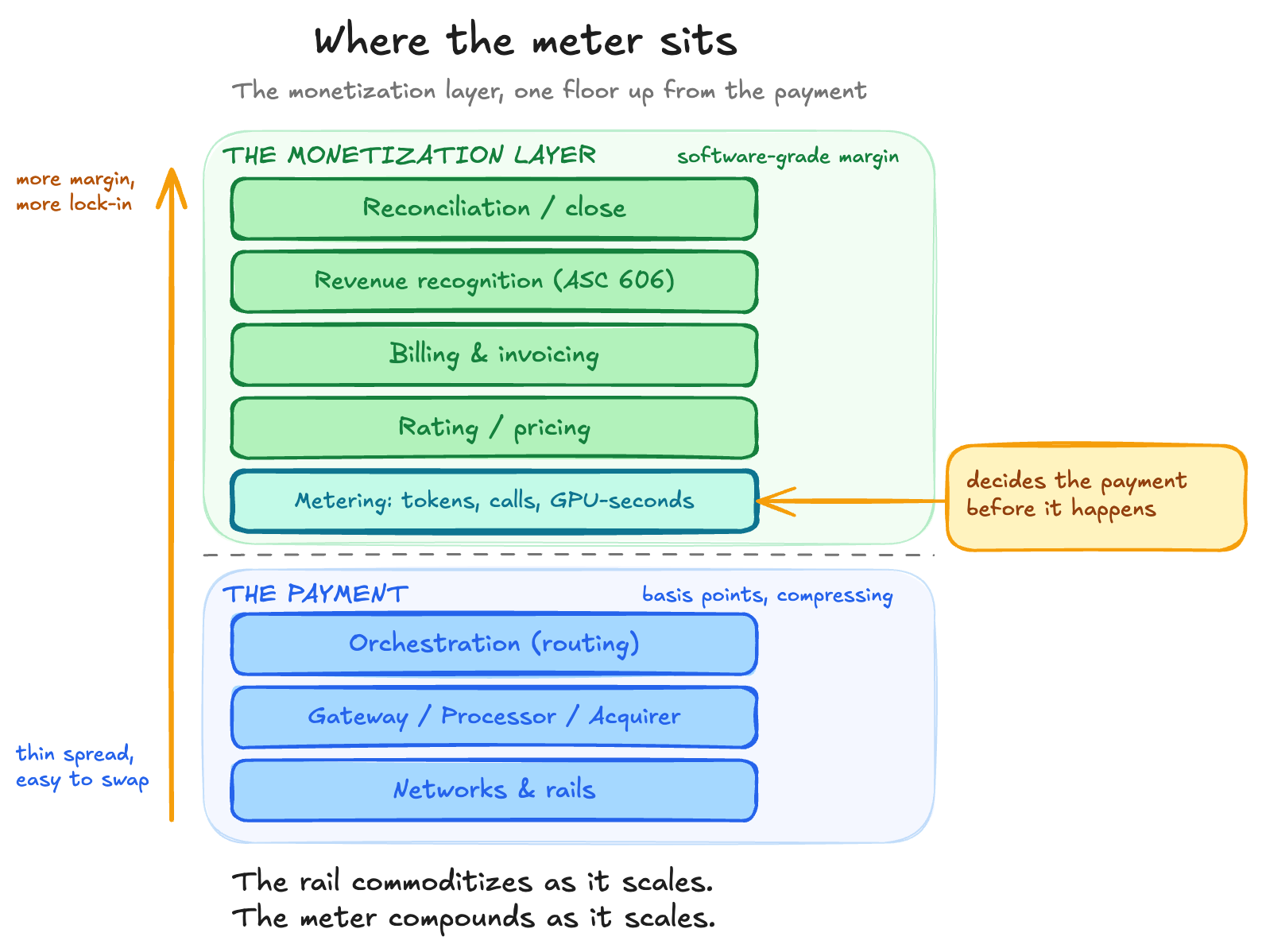

The monetization layer sits on top of the payment stack. It does five jobs:

Metering: captures raw usage, the tokens, API calls, and GPU-seconds a customer burns through.

Rating: turns those events into amounts, under whatever pricing logic you’ve set.

Billing: produces the invoices, credits, and caps.

Revenue recognition: books it all under ASC 606 and IFRS 15.

Reconciliation: closes the books.

Picture the stack (see diagram below). Networks and rails at the bottom, priced in basis points. Gateway, processor, and acquirer above them, also basis points, also compressing. Orchestration in the middle, thin and neutral.

Then a line. Below it is “the payment.” Above it is the money: metering, rating, billing, revenue recognition, and reconciliation.

Orb’s CEO, Alvaro Morales, makes the case plainly. Standalone billing systems, he says, are “fundamentally limited because they operate blind to transaction execution.”

The acquirers are betting the opposite. Fuse the two layers, and billing and payments are worth more together than apart.

One last point about that layer, and it’s the whole reason it matters. It’s where the price gets set. Everything below it just moves money. This is where you decide how much money there is to move.

Of those five jobs, metering is the hard one to build at scale. It’s the piece these deals were really chasing.

Why now, and not three years ago

For thirty years, software was sold by the seat. That model rested on one assumption: each extra user cost the vendor close to nothing.

AI killed the assumption.

Every model request costs real money. Tokens, GPU time, inference, all of it variable, all of it landing on the vendor’s own bill the moment it happens. When a customer fires 50 requests per minute, someone is paying for 50 requests per minute.

Run the per-seat math against that. If one AI agent does the work of ten people, you’ve sold one seat where you used to sell ten. Per-seat pricing undercharges for the value and leaves the vendor exposed to costs with no ceiling. It’s the worst of both: capped upside, uncapped cost.

Take a fifty-seat support team replaced by one AI agent that resolves tickets on its own. You’ve lost forty-nine seats of revenue and kept all of the costs. Intercom charges about a dollar per resolved ticket for exactly this reason: the value is in the tickets closed, not the seats filled.

The only way to line price up with cost is to meter what gets used.

You don’t need a survey to see where this is going. Watch the incumbents reprice their own products.

Salesforce charges for its Agentforce agents by the action, about ten cents each, through what it calls Flex Credits. GitHub moved every Copilot plan onto usage credits. Microsoft sells Copilot Studio in credit packs. Adobe meters its AI image generation the same way.

The firms with the most to lose from killing per-seat pricing are the ones killing it first. And the buyers are asking for it: enterprise procurement increasingly wants to pay for usage and outcomes, not seats nobody logs into.

Metronome’s surveys point in the same direction. Metronome’s 2025 study of usage-based pricing found that 77% of the largest software firms have already built consumption pricing into their products. Metronome sells billing software, so weigh it accordingly, but it matches what the incumbents are doing in plain sight.

The buyers say the timing out loud, too. Stripe calls metered pricing “the native business model for the AI era.” Adyen ties its move to the way AI is reshaping the way software is priced and consumed. Three buyers, one reason, no coordination.

Five deals, one target

Line the deals up, and the pattern is hard to miss.

Stripe bought Metronome, the metering engine behind OpenAI and Anthropic, for a reported $1 billion.

Adyen bought Orb, the billing platform for the AI-native crowd, for $335 million.

Salesforce bought m3ter and wired it straight into its CRM.

Airwallex bought OpenPay, then Leapfin, to cover billing all the way through to the closed books.

Five deals, four buyers, one year. That’s not a coincidence. It’s a market repricing a layer.

Notice who’s missing, too. Not one of these is a processor buying another processor. That game is being played elsewhere. This is scope, not scale.

Are they all buying the same thing?

From a distance, yes. Up close, no, and the differences are where it gets interesting.

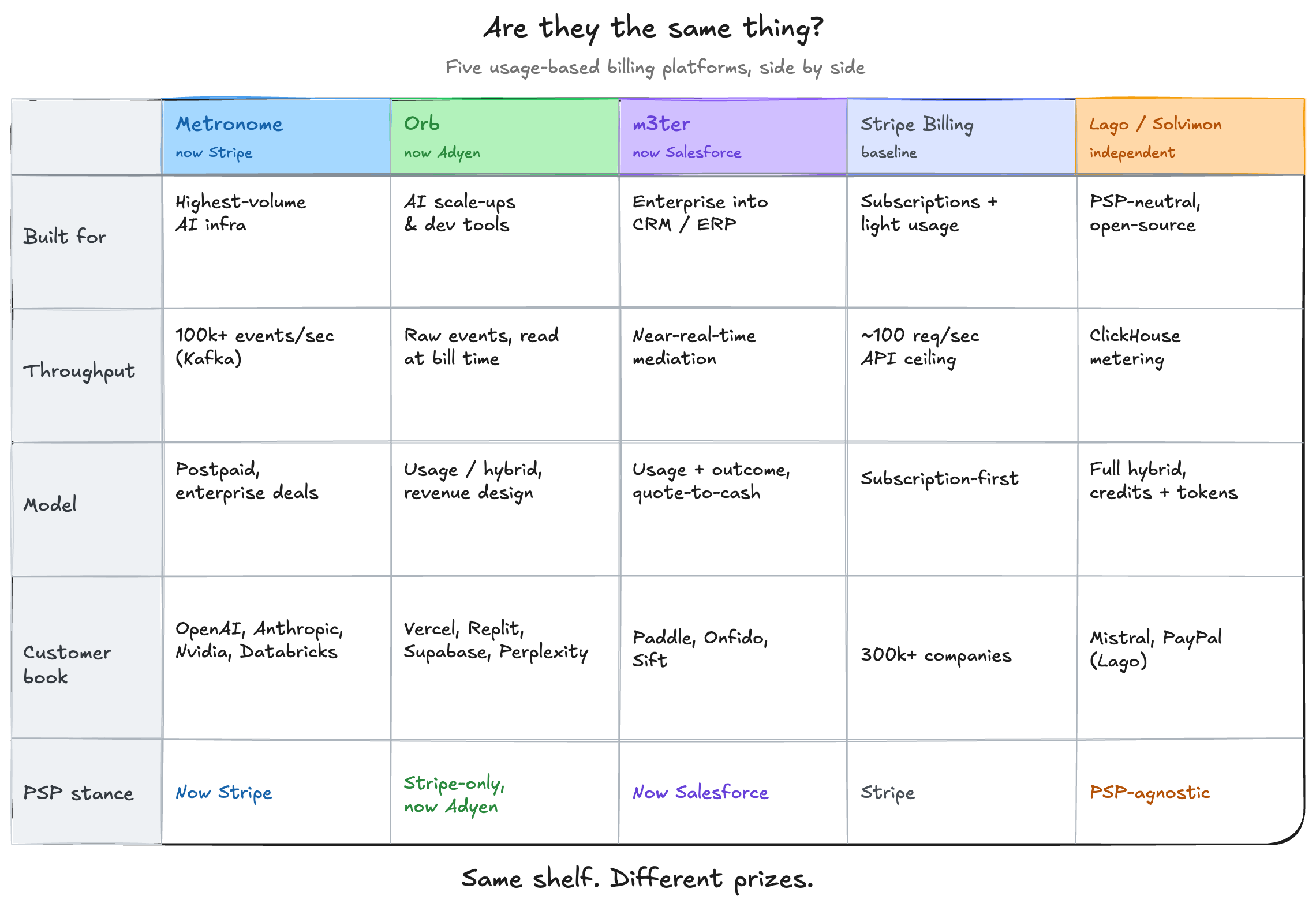

Metronome handles the heaviest volumes. It ingests more than 100,000 events a second on streaming infrastructure, and it ran the metering behind OpenAI, Anthropic, Nvidia, and Databricks before Stripe bought it. If your product bills by the token at frontier-AI scale, this is the one built for you.

Orb sits a notch in from there. It stores every raw usage event, then works out the bill by querying that history when the invoice runs. Because the raw events sit there untouched, you can change next quarter’s pricing and re-rate last quarter’s usage against it. Its customer list reads like the AI-native roster: Vercel, Replit, Supabase, Pinecone, Perplexity, and Glean.

Orb rebranded in January as a “revenue design platform.” That’s a dressed-up way of saying pricing should change as fast as the product does.

m3ter is the enterprise plumbing. Near-real-time metering and rating that feeds a company’s CRM, ERP, and quote-to-cash systems. Its customers include Paddle, Onfido, and Sift, and now it lives inside Salesforce.

Set those against Stripe Billing, which is subscription-first and, according to independent accounts, tops out at around 100 requests per second on its events API. That ceiling is the gap. AI products need a thousand times the headroom, which is roughly why Stripe wrote a reported billion-dollar cheque instead of shipping a patch.

Airwallex went furthest down the chain. It bought OpenPay for billing, then Leapfin for revenue recognition and reconciliation, the unglamorous work of turning a year of transactions into numbers an auditor will sign. Stitch those together, and you get one stack that runs from accepting the payment to closing the books. For a company that already moves money across borders for 250,000-plus businesses, that’s a pitch aimed at the finance team, not just the developer.

Salesforce is the tell that this isn’t only a payments story. It bought m3ter to give its customers usage billing inside the CRM. It also needs the meter to charge for its own AI: Agentforce runs on per-action credits and has already crossed a billion dollars in recurring revenue. When the buyer has to meter its own product to get paid, the layer isn’t optional.

So the buyers chose for different reasons. Stripe bought raw throughput and the Frontier-AI book. Adyen bought the scale-up book and a data loop. Salesforce bought a meter that speaks fluent CRM and can point at itself. Airwallex bought the whole lifecycle.

Same shelf. Different prizes.

The best builders in payments just became buyers

These aren’t companies that struggle to build software. So when all of them choose to buy instead of build, that tells you something.

Stripe built its own billing product back in 2018. It extended it for usage models. It even bought a small billing startup for its team in 2024. Then it paid a reported billion dollars for Metronome anyway.

That sequence is the evidence. If real-time, high-volume metering were a simple feature, Stripe would have shipped it. It bought instead, which tells you how hard the problem is.

Hard in a specific way. Metering at AI scale means swallowing a firehose of events without dropping any, storing them so you can re-price later, and rating them under pricing that changes every few weeks. Get one event wrong, and you’ve misinvoiced a customer who pays you millions a month. The people who can build this reliably are not in short supply.

Look at where the founders came from. Metronome’s are ex-Dropbox. Orb’s spent five years running engineering at Asana. m3ter’s spent three years inside AWS, watching how a hyperscaler bills usage at scale.

That’s a small, expensive talent pool, and the buyers paid for the teams as much as the code.

One detail here is hard to ignore.

The people who built Adyen’s own billing engine, the one that ran at over €970 billion in volume, left in 2022 to start Solvimon. They raised about €9 million from Northzone, they’re processor-agnostic, and they’re scaling. Adyen still chose to buy Orb, a US company, rather than rebuild on the talent it used to employ.

That’s not a knock on Adyen. It’s a measure of how specific the prize was.

Adyen wasn’t shopping for billing know-how. It was shopping for Orb’s AI-native customer base and for the speed of owning it now instead of in three years. You can build a billing engine. You can’t build someone else’s customer list.

What owning the meter actually gets you

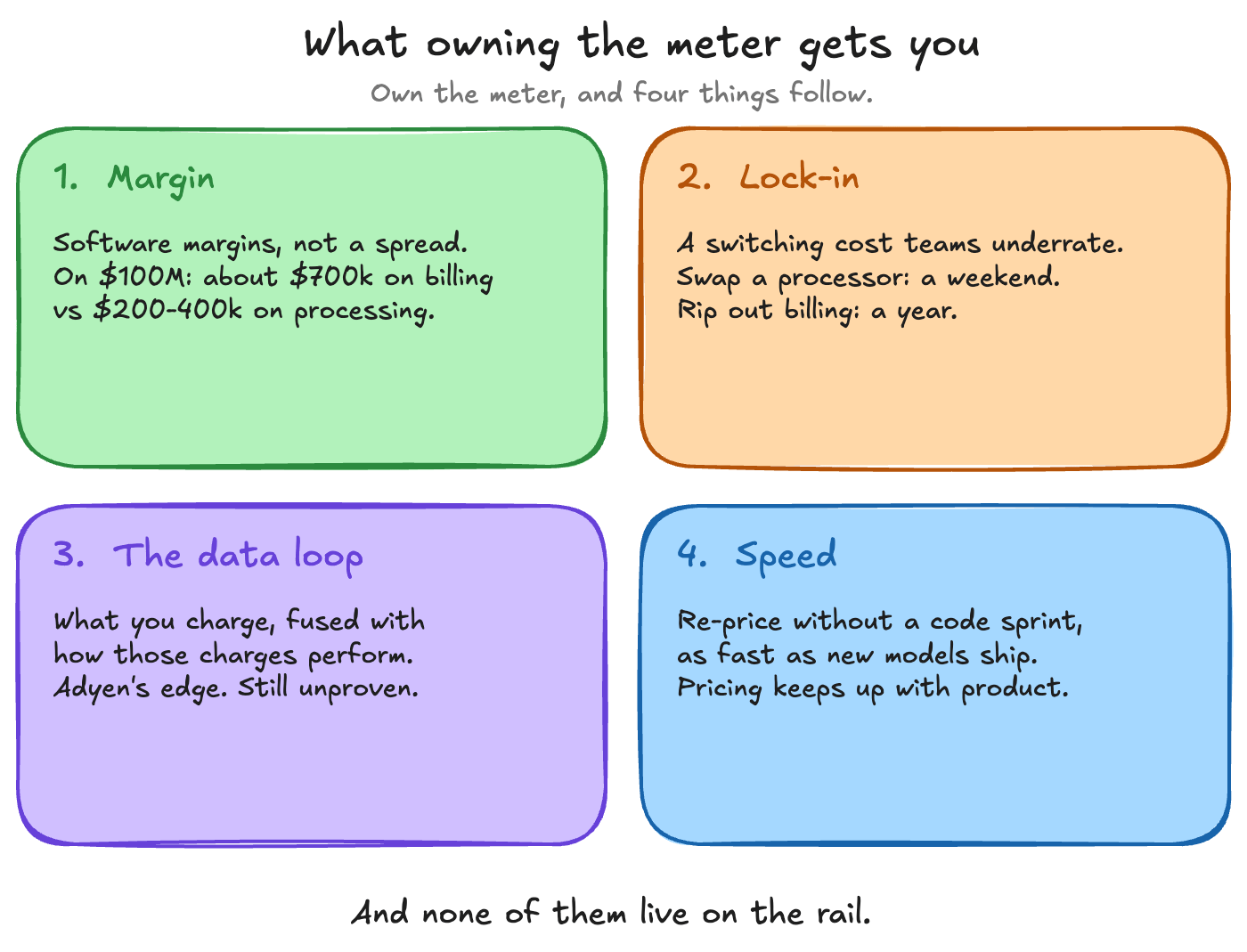

Four things, and they stack.

First, margin. Processing is a thin spread on a regulated cost. Billing software runs at software margins, roughly 80% gross, and the buyer can charge for it on top of the payment.

Stripe takes about 0.7% of billing volume on top of its processing fee, and its revenue-automation suite is on track for a billion-dollar run rate in 2026. The meter is a richer floor than the rail.

Run it on a merchant doing $100 million a year. As its processor, you might keep 20 to 40 basis points after interchange and scheme fees, so $200,000 to $400,000. Run its billing too, at 0.7% of the same volume, and that one line is $700,000, at software margins, on revenue far harder to walk away from.

Second, lock-in, and this is the real one. Swapping a payment processor is a weekend’s work by comparison, which is the entire reason orchestration layers exist. Ripping out a billing engine means re-wiring how you meter, invoice, book revenue, and pass an audit.

Once your processor also runs your billing, leaving stops being a project and becomes a year you don’t have. Ask anyone who has re-platformed billing. It’s measured in quarters, not weeks, and every quarter carries the risk of billing a customer incorrectly.

Third, the data loop. This is Adyen’s own framing, and it’s the sharpest of the four. Adyen described the Orb deal as closing the loop between what a merchant charges and how those charges perform.

In practice, that means seeing both the price a merchant sets and whether the resulting payment goes through, then using one to sharpen the other. A billing vendor that never touches the transaction can’t see the second half.

Done well, that could flag when a merchant’s heaviest users sit on its cheapest plan, or lift the success rate on recurring usage charges by retrying them more cleverly. Both are worth real money.

There’s a catch, though. No acquirer has yet to publish a hard number showing that the loop lifts authorization rates or reduces churn. The logic is strong. The proof is pending.

Fourth, speed. Whoever owns the meter lets a customer change pricing without booking an engineering sprint. In AI, where prices move every time a new model lands, that isn’t a luxury.

Mistral runs 32,000 invoices a month on per-token billing through Lago. Orb says Replit grew its revenue 40-fold after it moved onto usage billing. Those numbers break anything built for monthly subscriptions.

And one more the buyers rarely say out loud. Whoever meters OpenAI’s tokens gets a front-row view of how AI pricing behaves, across the whole market, before anyone else does.

One doubt worth holding

None of this is settled.

Stripe launched its own Billing product in 2018 partly to undercut the independents and fold billing into payments. The same move could turn billing into a near-free add-on and collapse the margin everyone is now paying for.

If that happens, the value climbs again, to whoever owns the next scarce layer: revenue intelligence, or the settlement of agent transactions. The meter is the prize today. It won’t stay the prize on its own.

What this means for you

Depends where you sit.

If you run a PSP or an acquirer, read this one twice. The per-transaction business is your floor now, not your ceiling. The question on the table is whether you can credibly offer the meter.

If you can’t, you become a commodity, rail-fed into someone else’s revenue system. The undifferentiated mid-market processor is exactly the spot everyone else is paying billions to leave.

If you’re a merchant, turn the question around. The headline reads “your processor wants to run your revenue,” and yes, that carries lock-in. The more useful question is whether your own pricing is keeping up.

Your customers increasingly expect usage and hybrid models. If your stack can’t meter and bill that, the processor offering to do it for you is solving a real problem, not inventing one.

It bites hardest in the mid-market, the merchants too big for self-serve and too small for white-glove. That’s the band where one accept-to-bill stack is most tempting, and where lock-in costs the most.

If you do hand it over, keep your options open. Hold your own usage data, keep more than one way to move money, and settle the exit terms before you’re in deep. The upside is speed. The risk is waking up unable to leave.

If you’re building in this space, the window for selling at the top just narrowed. The two best AI-native independents, Orb and Metronome, are gone. What’s left splits two ways.

There’s the neutral camp, betting that merchants will pay to keep billing independent of their processor. Lago, an open-source, multi-PSP platform, has raised over $22 million and runs billing for Mistral, PayPal, and Synthesia. Solvimon, the ex-Adyen team, took about €9 million from Northzone and stays processor-agnostic by design. Sequence raised around $19 million from Andreessen Horowitz on the same bet.

Then there’s the finance-first camp. Chargebee and Maxio are strong on subscriptions and revenue recognition for companies that care more about the close than the metering. Maxio came out of the SaaSOptics and Chargify merger; Chargebee keeps buying its way wider. Both are clean bolt-ons for an acquirer that wants billing without having to build it.

Any of them could be next. Checkout.com, PayPal, GoCardless, Fiserv, or Global Payments could all use a meter, and there are only so many good ones left.

Where this goes next

Watch four things over the next year or two.

A fifth big buyer is moving on a billing target. Billing revenue is growing faster than processing revenue. Any acquirer finally putting a hard number on that data loop. And the opposite signal, billing bundled toward free to win the payment, which would tell you the layer is commoditizing in turn.

By 2027, expect PSP pricing to shift. Less pure per-transaction basis points, more of a layered price: a platform fee to be there, a consumption fee on the meter above, and a thin processing spread underneath. The processor, still priced only in bps, is competing in the cheap seats.

There’s a thread back to the story everyone’s chasing, too. When AI agents start transacting on their own, paying per call and per outcome, the meter stops being a billing tool. It becomes the thing that settles the transaction.

The usage-based billing layer and the agentic-commerce layer are converging. The firms buying billing now are buying an early seat at that table.

One question for your next strategy session. Look at your stack and find the meter. Then ask who owns it.

If it’s the same company that moves your money, you’ve handed them the one box you can’t take back.

Thank you for reading.

P.S. If you’re reading this and are looking for the insights to help you improve your own strategy, that’s exactly what I help payments companies figure out.

20+ years in payments data and strategy. From being the First Data Scientist at Adyen, to being the First VP of Data Science & Analytics at Checkout.com, to helping over 50 of the top 150 acquirers and issuers globally, through my consultancy.

For Advisory. Speaking. Consultancy. Email me or DM me to set up a call.

Or, if you just want to keep fueling these breakdowns and deep dives, buy me a coffee.