Payments Strategy Cascade

Why “Coverage” Isn’t Strategy for PSPs, PayFacs and Acquirers

Here’s the uncomfortable truth I keep running into.

Most PSPs can explain their roadmap. They can’t explain their strategy.

They’ll tell you which payment methods they’re adding next. They’ll show you the new dashboard. They’ll talk about “expanding coverage” as if it were a plan.

In 2026, that’s how you end up building a very impressive product that sells at a very unimpressive margin.

Last week, in “Why Payments Strategy Matters”, I argued that we’re entering an infrastructure shift, not a feature cycle.

AI agents moved from demos to production. Tokenization moved from security add-on to default plumbing. Stablecoins moved from trading to settlement. Cloud processors kept replacing batch-era systems.

Each one matters on its own. Together, they change what “advantage” looks like in payments.

The data backs that up.

Visa has already provisioned 12.6 billion network tokens. Stablecoins processed $26 trillion in on-chain volume. Those aren’t niche experiments anymore, they’re scale signals.

And unlike the EMV transition, which dragged on for years, this one is moving fast. The companies that treat it as a product backlog will wake up to find the economics have shifted beneath them.

This week's newsletter is the missing piece to last week’s newsletter, which was read over 10.000 times!

If last week was the why, this is the how.

Not a “how to write a strategy deck.” But rather, how to make choices that survive price compression.

Because the traditional PSP playbook is failing for one simple reason.

Payments got cheaper. Complexity did not.

When you can buy “good enough” acquiring from half the market, you don’t win by adding more “good enough.” You win by being meaningfully better at one system that compounds.

That’s the entire game.

So I’m going to adapt one of the cleanest strategy frameworks I know, Playing to Win, and apply it to the reality of PSPs and PayFacs.

No theory. No vendor buzzwords. No pretending every company should do the same thing.

Just five choices, and to give it more depth, I have chosen to work out how I would apply this to a PayFac.

Let’s dive in.

What Strategy Is, in One Sentence

Strategy is a coherent set of choices about where you’ll play and how you’ll win.

It’s not your goals. “Grow TPV 30%” is an outcome, not a strategy.

It’s not your roadmap. A roadmap is what you plan to build. Strategy is why those builds translate into an advantage.

Founders love optionality. The market punishes it.

What changed in 2025 and 2026 is not that building payments became impossible.

It’s that being average became lethal.

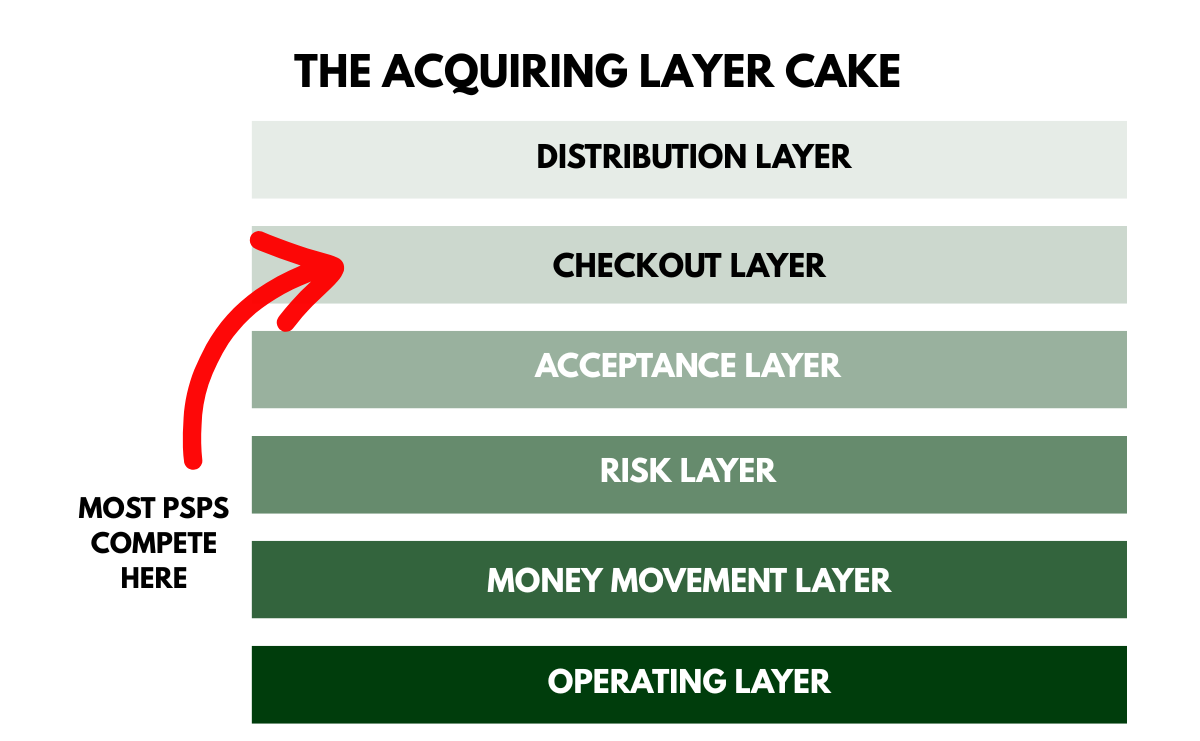

The Acquiring Layer Cake

Most PSPs talk about “payments” as if it’s one product. It’s not. It’s a stack, and the layer you compete in determines whether you end up in a race to the bottom.

Here’s the simplified layer cake for PSPs and PayFacs.

Distribution layer: how merchants show up in your funnel, direct sales, or embedded into platforms

Checkout layer: gateway UX, method mix, credential handling, tokenization

Acceptance layer: acquiring setup, routing, retries, issuer performance

Risk layer: underwriting, monitoring, disputes, chargebacks

Money movement layer: settlement, payouts, reconciliation

Operating layer: support, incident response, controls, cost-to-serve

Most early-stage PSPs try to differentiate in the checkout layer.

That’s the layer competitors can copy the fastest.

PayFacs win or lose in distribution, risk, and operations. That’s where the compounding happens, and where most companies arrive late.

Now we can talk strategy.

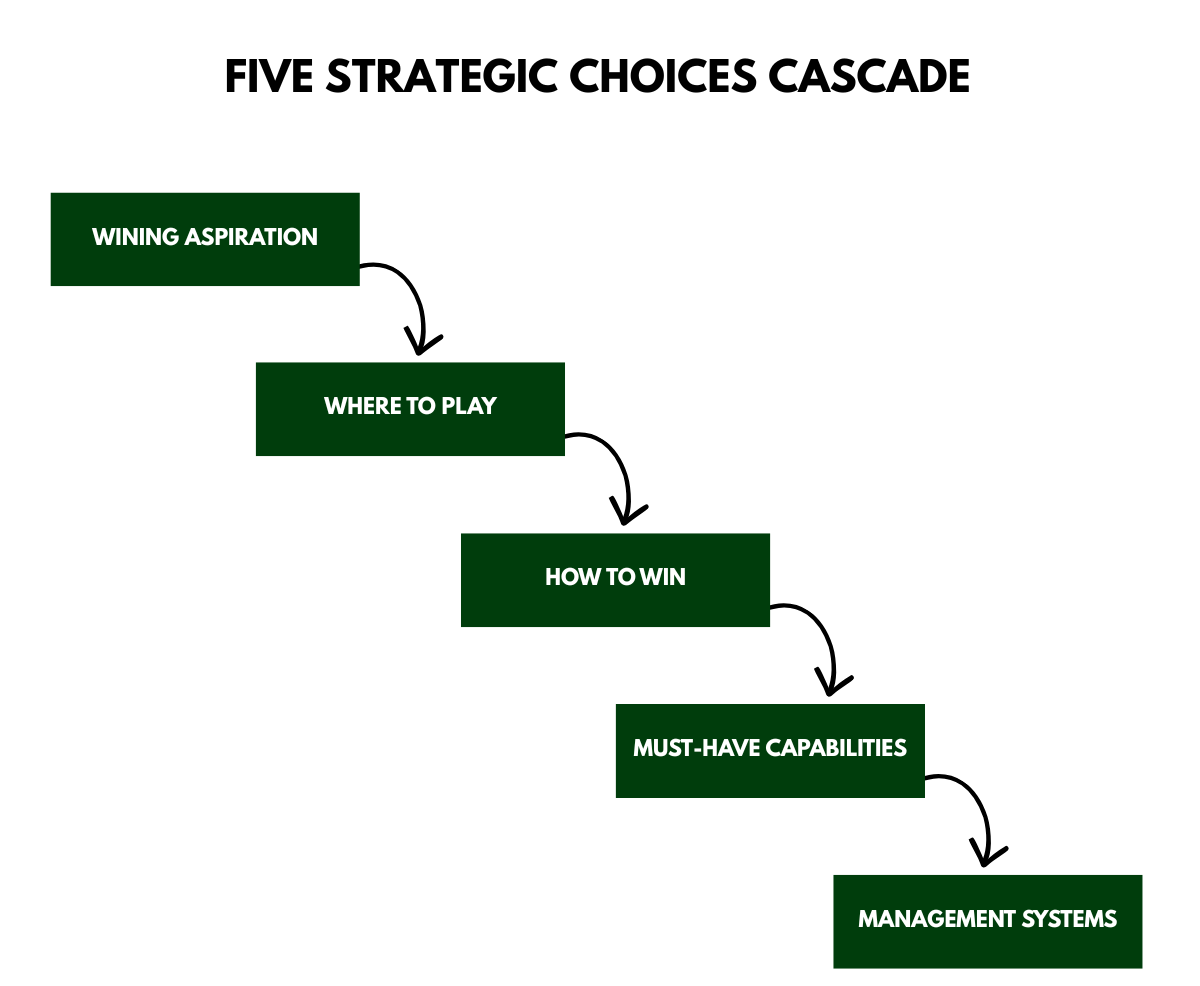

The PSP and PayFac Strategy Cascade

Playing to Win forces five integrated choices.

Winning aspiration,

Where to play,

How to win,

Must-have capabilities,

Management systems.

Answer them in order, and you stop drifting. Skip one, and your company fills the gap with vibes.

Let’s translate each choice into acquiring reality.

Choice 1: Winning Aspiration, Acquiring-Native

Most PSPs default to “we want to grow.” That’s fine. It’s not useful.

A winning aspiration is the outcome you want that forces trade-offs.

In acquiring, “winning” is the ability to defend the margin while volumes scale.

So your aspiration needs to be specific about what you’re trying to be best at.

Do you want to be the default payments layer for a specific platform ecosystem?

Do you want to win enterprise deals because you’re measurably better on approvals and reliability?

Do you want to build a PayFac engine that can onboard and monitor merchants profitably at scale, without drowning in ops?

If your aspiration doesn’t make you uncomfortable, it’s probably not a choice.

Choice 2: Where to Play, the Battlefield

“Where to play” is not your TAM. It’s the subset of the market where your model can win.

In PSP and PayFac land, your playing field is defined by a few axes that matter more than the slideware.

Customer type: SMB direct, embedded platforms, mid-market, enterprise

Vertical focus: one to three categories where you can build a repeatable playbook

Geography: where you can actually operate KYB, payouts, and support, not just sell

Merchant risk profile: the risk you’re willing and able to carry

Channel: direct sales versus embedded distribution

Operating model: PSP, PayFac, or something in between

There’s a PayFac question that forces honesty.

Are you a distribution company that happens to do payments, or a payments company trying to buy distribution?

If your answer is “both,” you’re probably building complexity faster than you’re building advantage.

Choice 3: How to Win, the Part Most Teams Avoid

Most companies answer “how to win” with a feature list.

Tokenization, orchestration, AI, stablecoins, local methods, one-click checkout.

That’s not a strategy. That’s a shopping list.

“How to win” is your advantage logic, the reason you beat a competent competitor in your chosen field.

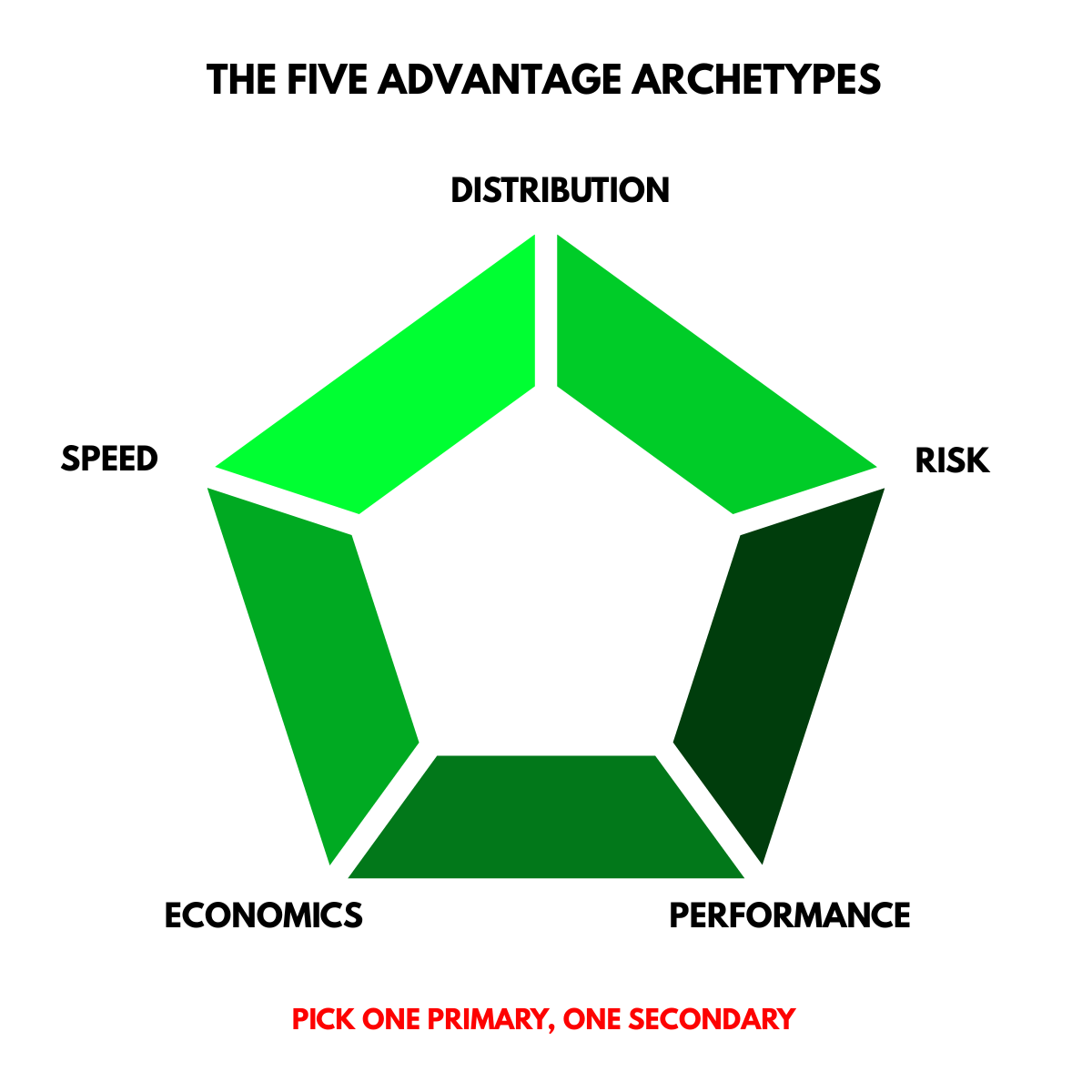

For PSPs and PayFacs, most real “how to win” answers fit into a small set of archetypes.

Distribution advantage, risk advantage, performance advantage, economics advantage, speed-to-value advantage.

They’re not slogans. They’re operating realities.

Distribution advantage means you win before the merchant ever “chooses” a PSP, because you’re embedded in the platform they already run their business on.

Risk advantage means you can approve, price, and monitor merchants profitably in segments where others either say no, or say yes and regret it.

Performance advantage means you can point to measurable outcomes. Higher approvals, fewer false declines, less downtime, fewer avoidable failures in payouts and settlement.

Economics advantage means you can keep cost-to-serve low, and pricing disciplined, while competitors keep adding humans to cope with their own complexity.

Speed-to-value advantage means merchants go live faster, and see value faster. Not because your team heroically jumps on calls, but because your defaults and tooling remove friction.

Pick one as primary. Pick one as secondary.

If a competitor with more capital copied your product in six months, what would still be true about why you win?

That’s your strategy.

Here’s the quiet part.

Commoditization in acquiring doesn’t happen when you stop innovating. It happens when your “innovation” only changes the checkout layer.

If your differentiation lives in the UI, your competitor can copy it. If it lives in distribution, risk, and operating systems, copying it takes years, not weeks.

That’s why the same feature can mean two different things.

Tokenization is a checkbox for a generic PSP. It’s a lever for a PSP whose strategy is performance, because credential quality and lifecycle management can directly move approvals.

Stablecoin settlement is a headline for a generic PSP. It’s a lever for a PSP whose strategy is economics, because settlement and treasury are part of the margin story.

Same trend. Different strategic meaning.

Choice 4: Must-Have Capabilities, the Few That Matter

Capabilities are not ideas. They’re repeatable strengths that show up under stress.

In payments, the stress test is always the same. Volume spikes, fraud patterns shift, a partner tightens rules, and your support queue fills up.

This is where founders blow it by listing twenty things they want to be good at.

If everything is a must-have, nothing is.

For PSPs and PayFacs, the capabilities that tend to matter look like this.

Onboarding throughput with exception handling. A real flow that doesn’t collapse when the first messy cases show up.

A risk engine with operating playbooks. Limits, monitoring, interventions, and escalation paths that work at 10 merchants and at 10,000.

Disputes and chargebacks as a system. Pre-dispute, evidence capture, workflow, and learning loops.

Reconciliation truth. Clean data, clear statuses, and tooling that makes ops faster, not louder.

Payout reliability. Failure handling, predictable settlement, and a support model that doesn’t become your biggest department.

Routing governance. Controlled experiments, measured changes, and an ability to separate real uplift from noisy luck.

Reliability discipline. Incident response, release gates, and postmortems that prevent repeat incidents.

If you’re building a PayFac, your moat is rarely “payments.” It’s underwriting, monitoring, and operations at scale.

That’s not glamorous. It’s profitable.

Choice 5: Management Systems, How Strategy Survives Q2

Strategy dies when incentives and cadence reward the wrong work.

In acquiring, the wrong work looks like chasing marginal deals because the top-line feels good, and quietly accepting margin decay as “the market.”

Management systems are how you stop that drift.

Start with segment-level unit economics you can trust. A margin waterfall by platform, vertical, cohort, or region, not an average that hides the truth.

If you don’t have that waterfall, you can’t see what’s actually driving margin. You’ll argue about pricing while your cost-to-serve quietly becomes the real problem.

Add guardrails for loss rates and dispute rates that tighten or loosen without a weekly crisis meeting.

Put change control around risk rules and routing. Somebody owns it. Impact gets measured. Rollback stays easy.

Keep build versus buy discipline. Partnerships are not free. Every integration is a maintenance tax.

And run a churn truth loop. Not the polite version, the real one.

Build these systems early, or build them later under pressure. The second option costs more.

A Worked Example: The Vertical SaaS PayFac Path

Let’s make this concrete.

Here’s a strategy that I have helped several PSPs develop to pivot away from the classic “generic PSP” model.

A vertical SaaS PayFac for field services.

Think plumbers, electricians, HVAC, and other businesses that live in scheduling software, not spreadsheets.

In this world, payments is part of the operating workflow. Invoices go out, jobs get completed, deposits get collected, and payouts happen.

The merchant doesn’t want a “payments dashboard.” They want less admin.

That context is the strategy seed.

Now watch how the cascade forces focus.

Winning Aspiration

Become the default monetization layer for field-service platforms in Europe, using payments to increase retention for the platform and reduce admin work for merchants.

It’s not “be the best PayFac.” It’s not “go global.” It’s a specific ambition tied to a specific distribution path.

Where to Play

Customers are vertical SaaS platforms, not direct SMBs.

The vertical is field services and home services, not “any small business.”

Geography is Europe where you can actually run KYB and payouts reliably.

Channel is embedded distribution only. No direct SMB sales motion.

That last line is where most founders flinch.

But it’s what makes the model coherent. Direct SMB sales turns you into a marketing company. Embedded distribution turns you into a platform partner.

Different economics. Different skills. Different support model.

How to Win

Primary advantage is distribution. You win because you’re where the merchant already works.

Secondary advantage is risk. You win because you can underwrite and monitor aggregated merchants better than the platform can, and better than generic PSPs can at this scale.

Must-Have Capabilities

Onboarding throughput with exception handling. KYB automation, plus a clean path for the messy cases.

Monitoring and interventions. Limits, triggers, and rapid-response playbooks built for aggregated merchants.

Disputes workflows built into the product. Evidence capture is not a PDF hunt. It’s a button the merchant can press inside the workflow.

Payout and reconciliation reliability. If payouts fail, the platform gets blamed, and you get fired.

In embedded payments, reliability is distribution.

Management Systems

Cohort economics by platform and vintage. Profitability is segmented, not averaged.

Automated risk guardrails. Tighten or loosen limits based on signals, without a daily human debate.

Concentration reviews. Platform dependency is a strategic risk, not a nice problem to have.

And then the most important part, the one most payments companies avoid writing down.

The No list.

No direct SMB sales.

No “global coverage” until the operating model is proven.

No high-risk categories until risk ops is mature.

That’s what turns a plan into a strategy.

The trap most payments companies fall into is thinking “no” closes doors.

It doesn’t. It stops you from building doors that open into brick walls.

How to Use This This Week

If you want to turn this into action, run a 60-minute Management session.

Write your winning aspiration in one sentence, then sharpen it until it implies a no.

Define where to play across the axes, and circle what you will not pursue this quarter.

Pick your primary “how to win” archetype, and write it as a logic statement, not a feature list.

List the three capabilities you’ll bet on, and the two you will deliberately ignore.

Decide which management system you’ll implement first: margin waterfall, risk guardrails, routing governance, or churn truth.

That’s it.

Strategy doesn’t need to be complicated. It needs to be coherent.

And when the next trend arrives, treat it as a test.

Does it strengthen your advantage logic, or commoditize it?

If you can’t answer that, your roadmap is leading your strategy, not the other way around.

What This Means for the Team Inside a PSP or PayFac

If you’re the CEO, reward focus that compounds, even when it looks boring on a demo call.

If you run product and engineering, build systems that survive stress: onboarding, reconciliation truth, risk ops, and reliability.

If you run risk and ops, you’re not a cost center. You’re the business model.

If you run sales or partnerships, qualify deals by where-to-play fit, not promised volume.

If you run finance, enforce margin truth by segment. Kill zombie segments early.

The One-Page Template

Winning aspiration:

Where to play:

How to win:

Must-have capabilities:

Management systems:

90-day No list:

If you can’t fill that in without arguing, good. That means you’re close to doing strategy instead of theatre.

Coverage is optional.

Choices aren’t.

Thank you for reading.

P.S. If you are looking for a Payments Strategist to help you with figuring out what to focus on, or organizing an event, webinar where you need someone to educate and or challenge your audience on what’s happening in payments, please don’t hesitate to email or DM me, to set up a call.

Or if you appreciate my work, feel free to buy me a coffee!