Payments Orchestration

How enterprise merchants unlock higher approvals and lower costs by conducting their own payment symphony.

For most enterprise merchants, the realization hits during a board meeting. The CFO points to a line item showing 2.9% payment processing fees on $200 million in volume. That's $5.8 million annually, before considering the revenue lost to failed transactions.

Meanwhile, the head of engineering explains why adding a local payment method in Brazil will take six months through their current provider. At the same time, the marketing team wants to test a new checkout flow, but the PSP's hosted payment page solution doesn't support the required customization.

At this moment, enterprise merchants discover they've outgrown the single-provider model that served them well as a startup.

They need something more sophisticated: a payments orchestration platform that turns them from passive consumers of payment services into active conductors of their own payment symphony.

In this edition of the Payments Strategy Breakdown, I'll explain why payments orchestration has become the preferred model for enterprise merchants processing over $100 million annually.

To achieve this, I have partnered with IXOPAY to provide an in-depth example of how merchants can connect with over 200 payment providers through a single integration. I will also highlight the hidden costs of provider lock-in and why the most successful merchants are choosing an orchestration layer as their basis for building their own composable payment stacks.

Let's dive in...

The Single-Provider Ceiling

When Stripe launched in 2010, their seven-line integration became the gold standard for payment simplicity. Merchants can accept cards globally without managing multiple relationships, reconciling different settlement files, or building their own fraud detection systems.

This model works perfectly until scale introduces complexity.

For example, a $200 million-a-year revenue e-commerce retailer discovers that their authorization rates vary dramatically by region. Cards issued in Germany are approved at a rate of 89% through their current PSP, while the same provider delivers only 81% approval rates for Italian cards. The difference costs them $3.2 million in annual lost revenue.

Their PSP explains that routing optimization "is on the roadmap." The merchant realizes they're hostage to another company's priorities.

Meanwhile, their subscription business faces involuntary churn when cards expire. Network tokens could reduce this by automatically updating credentials, but their provider hasn't implemented the feature. Their SaaS competitors, who use dedicated billing platforms, report 15% lower churn rates.

The breaking point arrives when they expand into Latin America. Their PSP doesn't support PIX, Brazil's dominant payment method. Adding it requires waiting for a provider roadmap item while competitors capture market share with localized checkout experiences.

This is an example I come across multiple times per month, as I discuss Payments with Enterprise merchants.

The truth that many might not want to acknowledge is that single providers optimize for their own economic interests, not yours.

What Orchestration Actually Solves

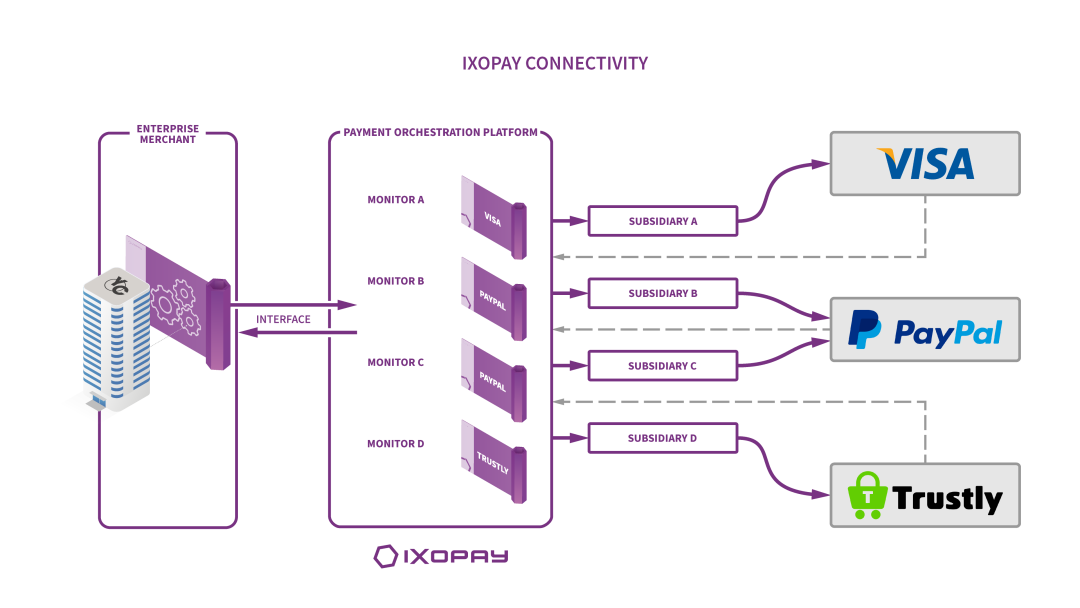

Payment orchestration platforms, such as IXOPAY, act as a central nervous system for enterprise payment operations.

Instead of being locked into one provider's capabilities, merchants can connect to dozens of specialized services and route each transaction to the optimal endpoint.

The architecture resembles a sophisticated air traffic control system.

Each transaction arrives with specific characteristics: card type, issuer country, transaction amount, and customer risk score. The orchestration engine evaluates these attributes against real-time performance data and business rules, then routes the payment to the provider most likely to approve it at the lowest cost.

IXOPAY currently connects to over 200 payment providers and methods globally.

While that many integrations might seem like a lot, the idea behind it is not just about having options; it's about having the right option for each specific transaction.

For example, a German luxury retailer using orchestration might route domestic Girocard transactions through a local acquirer offering 1.2% fees, while sending high-value international purchases through a provider specializing in premium fraud detection.

American Express cards could be routed to a processor offering better Amex rates, while subscription renewals utilize network tokens through the provider with the highest success rates for recurring payments.

The merchant maintains one integration while accessing specialized capabilities from multiple providers.

The economics become compelling quickly.

Merchants report a 2-4% improvement in authorization rates after implementing orchestration. On $200 million in volume, that's $4-8 million in recovered revenue annually. Even after paying orchestration platform fees, the ROI often exceeds 300% in the first year.

The Hidden Costs of Provider Lock-In

Having worked with hundreds of Enterprise merchants on Auditing and Optimizing their Payments Performance, one thing has always stood out to me.

Enterprise merchants underestimate the true cost of single-provider relationships until they attempt to switch.

While many look at it from a purely processing costs perspective, I believe several other essential factors need to be considered when evaluating the true costs of a single provider, when deciding to switch.

Data portability becomes the first challenge.

Many providers use proprietary token formats that are not transferable to competitors. A merchant with 50,000 stored payment methods might need to ask customers to re-enter their cards, causing significant churn during the migration.Feature gaps compound over time.

Your provider might excel at fraud detection but lag in emerging payment methods. By the time they support digital wallets or buy-now-pay-later options, competitors have gained 18 months of market advantage.Pricing leverage disappears once you're deeply integrated.

Providers know that switching costs are high, which reduces their incentives to offer competitive rates as their volume grows. Some merchants discover they're paying premium fees for commodity services simply because renegotiation is easier than migration.Geographic limitations restrict expansion.

Your PSP might not support strong customer authentication in Europe or lack local acquiring relationships in Asia. Each missing capability forces workarounds that increase complexity without adding value.

Orchestration platforms are designed to solve these problems.

Universal token vaults store payment credentials in network-standard formats that work across providers. Merchants can test new services without replacing their entire stack, and pricing negotiations become competitive auctions rather than captive renewals.

Beyond Routing: The Composable Payment Stack

Modern orchestration platforms extend far beyond transaction routing.

They've evolved into comprehensive payment operating systems that let merchants compose best-of-breed capabilities.

Let’s break down the IXOPAY platform to see which benefits it provides.

Universal tokenization represents the foundation.

IXOPAY's recent merger with TokenEx demonstrates the strategic importance of provider-agnostic token management. Merchants can store payment credentials once and use them across any connected processor, eliminating the vendor lock-in that traditional tokenization creates.

Intelligent 3D Secure management optimizes authentication flows.

Rather than applying uniform rules, the platform can route high-risk transactions through strict authentication while exempting trusted customers. Some implementations achieve a 40% reduction in authentication challenges without increasing fraud rates.

Fraud prevention becomes modular.

IXOPAY's partnership with Riskified enables merchants to integrate specialized AI-driven fraud detection without replacing their entire payment stack. They can test multiple fraud vendors simultaneously, routing different transaction types to the most effective solution.

Reconciliation and reporting consolidate data from dozens of sources.

Instead of managing separate dashboards and settlement files from each provider, merchants get unified views of payment performance, costs, and customer behavior patterns.

Network token management happens automatically.

The platform can request tokens from Visa, Mastercard, and other networks, then deploy them across whichever processor offers the best rates for tokenized transactions. Merchants report 2-3% authorization rate improvements and reduced interchange costs without changing their checkout experience.

For Enterprise merchants, platforms like IXOPAY become an invisible infrastructure that makes every other payment service more valuable.

Enterprise Implementation Strategy

While choosing a great orchestration platform is the first step, successful orchestration is based on implementation, which follows a predictable pattern.

From my experience, smart merchants start with specific pain points rather than attempting comprehensive replacements.

Here are the four phases an Enterprise merchant goes through when successfully implementing an orchestration platform.

Phase one typically focuses on geographic expansion or adding alternative payment methods. A merchant expanding into Europe may connect with a local SEPA Direct Debit provider while maintaining their existing credit card processing. This proves the orchestration concept without disrupting core operations.

Phase two introduces intelligent routing for credit card transactions. Merchants connect a second acquirer and begin A/B testing transaction allocation. Early results typically show a 1-2% improvement in authorization rates, building internal confidence in the platform's value.

Phase three adds specialized capabilities: fraud detection, subscription management, or network tokenization. Each new service integrates through the orchestration layer, avoiding the complexity of direct vendor management.

Phase four implements full optimization: dynamic routing based on real-time performance, cost optimization across providers, and automated failover during outages. Advanced merchants achieve authorization rates 3-5 percentage points above single-provider baselines.

The key insight is treating orchestration as an evolution, not a revolution.

Merchants who attempt immediate full-stack replacements often struggle with complexity. Those who add capabilities incrementally build expertise while reducing risk.

Understanding the Impact of Payments Orchestration Through Numbers

To provide a clearer picture of the impact of an orchestration platform, let’s go through the numbers.

For example, a European marketplace processing $500 million annually faced classic scaling challenges.

Authorization rates varied from 85% in domestic markets to 71% in Latin America.

Payment costs averaged 3.2% of gross merchandise value.

Customer complaints about failed transactions increased 40% year-over-year.

To transform their business and overall payments performance, they implemented an orchestration platform connecting to local acquirers in each market.

Brazilian transactions are routed to a provider supporting PIX and Boleto.

Mexican payments used local bank relationships for better approval rates.

European transactions initially remained with their existing acquirer.

Results appeared within 30 days.

Brazilian authorization rates improved from 71% to 84%, while Mexican approvals increased from 75% to 88%.

The marketplace recovered approximately $180,000 in monthly revenue from previously failed transactions.

Phase two introduced intelligent fraud detection.

High-risk transactions are routed through Riskified's machine learning platform, while trusted customers enjoy a frictionless checkout experience.

Fraud rates decreased by 28% while authorization rates improved by an additional 1.5%.

Phase three implemented network tokenization across all markets.

Card-on-file transactions utilized network tokens when available, resulting in reduced decline rates for subscription renewals and repeat purchases.

Monthly revenue recovery reached $340,000.

The total implementation required eight months and cost $150,000 in platform fees and integration work.

Monthly savings now exceed $500,000, delivering a 400% return on investment (ROI) while positioning the marketplace for continued growth.

When Orchestration Makes Sense

Not every merchant benefits from payment orchestration. The model works best for companies with specific characteristics and challenges.

Transaction volume represents the primary qualifier.

Merchants processing under $50 million annually rarely justify the complexity (but I have seen cases where it does). Those above $100 million almost always benefit from optimization opportunities.

Geographic diversity amplifies orchestration value.

Companies selling globally face varied local payment preferences, regulatory requirements, and acquirer performance. Single providers excel in their home markets but often struggle with international optimization.

Product complexity matters significantly.

Marketplaces managing split payments, subscription businesses fighting involuntary churn, and platforms enabling embedded finance need specialized capabilities that general-purpose providers struggle to deliver.

Engineering sophistication determines implementation success.

Orchestration requires technical teams comfortable with API integration, webhook management, and monitoring multiple service relationships. Companies lacking payment expertise should build internal capabilities before adding orchestration complexity.

Risk tolerance influences platform selection.

Orchestration introduces new failure modes: routing logic errors, provider outages affecting specific transaction types, and reconciliation complexity across multiple settlement sources. Merchants must balance the benefits of optimization against the operational complexity.

The strongest candidates are growing enterprises with payment-savvy teams facing clear performance gaps in their current setup.

Building Your Orchestration Strategy

Enterprise merchants considering orchestration should approach the decision systematically rather than reactively.

First, audit current payment performance.

Analyze authorization rates by geography, card type, and transaction amount. Identify areas where performance can be improved through specialized providers or local acquisition relationships.

Second, calculate the opportunity cost.

Every percentage point of authorization rate improvement translates directly to revenue recovery. Model the financial impact of realistic improvements against implementation costs and ongoing platform fees.

Third, assess internal capabilities.

Orchestration requires dedicated payment expertise, integration bandwidth, and ongoing operational management. Merchants lacking these resources should prioritize team development before selecting a platform.

Fourth, define success metrics.

Authorization rates, processing costs, and customer experience scores provide quantifiable targets for improvement. Establish baselines and improvement goals before implementation begins.

Fifth, plan an incremental rollout.

Start with specific geographies, payment methods, or customer segments. Prove value in controlled environments before expanding the scope. This approach reduces risk while building internal expertise.

Sixth, evaluate vendor fit.

Orchestration platforms differ significantly in their strengths, integration approaches, and commercial models. Match platform capabilities to your specific requirements rather than choosing based on general reputation.

The goal is to treat orchestration as a strategic infrastructure that evolves in tandem with business needs, rather than a tactical solution to immediate problems.

Looking Forward

Payment orchestration represents the natural evolution of enterprise payment management. As digital commerce becomes increasingly global and complex, merchants need infrastructure that adapts rather than constrains.

The next generation of orchestration platforms will incorporate more sophisticated decision-making. Machine learning models will optimize routing in real-time based on changing provider performance. Predictive analytics will anticipate payment failures before they occur. Integration with emerging payment methods will happen automatically as new rails become available.

Smart merchants are positioning for this future by building flexible payment architectures today. Those who wait for perfect solutions will find themselves perpetually behind competitors willing to invest in payment optimization.

The question isn't whether to implement orchestration, but when and how to do it strategically.

Enterprise merchants processing significant volumes with complex requirements have already made the transition. Those still relying on single providers should evaluate whether their current approach supports their growth ambitions.

In the next edition, we'll examine PayFac-as-a-Service models and how software platforms are monetizing payments without becoming licensed financial institutions. We'll analyze Tilled's revenue-sharing approach and explore why embedded finance has become essential for platform businesses.

The shift from monolithic to composable payments continues accelerating.

Merchants who embrace this evolution will control their payment destiny. Those who resist will remain dependent on providers whose priorities may not align with their business objectives.

Build optionality into every payment decision today, and you can optimize tomorrow without having to start over.

Thank You for Reading. Please like, Comment, Share, or Post on Your Social media. I appreciate all the feedback I can get.

P.S. If you're interested in collaborating with me on a larger scale, whether through speaking, advisory services, or consulting, please don't hesitate to email or DM me.

P.P.S. A special thank you to IXOPAY for supporting me in creating this in-depth newsletter on Orchestration, by showing me firsthand what their platform does and how it helps enterprise merchants succeed.