Agentic Economics

Who Captures Value When AI Agents Control Spending

Until now, we can be thankful that the foundational protocols are free.

Stripe’s Agentic Commerce Protocol charges nothing, and neither does Google’s Agent Payments Protocol charge anything. Both operate under the Apache 2.0 open-source license with zero per-transaction fees.

Meanwhile, OpenAI charges merchants a “small fee” it won’t disclose. Industry estimates range from 0.5% to 2%. But no one knows for sure.

This gap between free protocols and opaque platform fees defines the economic battle ahead.

Every layer of the payments stack is trying to figure out where margin lives when the infrastructure itself is deliberately free. For payment professionals working at networks, processors, and infrastructure companies, this creates an urgent question:

How do you capture value when the protocols cost nothing, but platforms extracting fees won’t say how much?

If you read, Payments Protocols, you already understand the protocols.

I broke down the different protocols and the market-size projections that everyone is currently fighting hard to be part of.

What you need now is to understand the economics.

Who charges what.

Where fees stack.

Why some layers have pricing power while others face commoditization.

How value gets split across issuer, network, processor, platform, and protocol provider in this new world.

That’s what this newsletter is about.

An Economics 101 explainer on agentic commerce, written specifically for payment professionals who need to understand how their companies capture value when AI agents control spending.

Let’s dive in.

How payment economics work today

Let’s start with what you already know. When a consumer buys something online with a credit card today, here’s the economic breakdown on a $100 purchase:

The merchant pays $3.10 total (Extreme U.S. Example).

That $3.10 splits six ways.

The issuing bank captures $2.40 in interchange.

The card network takes $0.14 in assessment fees.

The payment processor and acquirer mark up $0.40 for its services.

Fraud detection adds another $0.16.

Each layer has a defined role, a standardized fee, and an established place in the value chain.

The merchant absorbs all of it. They’ve got no choice. If they want to accept cards, they pay the fee.

The economics are transparent. Interchange schedules are published. Network assessments are standardized. Processor rates are negotiated but comparable. Everyone knows who charges what and why.

This model works because of two things: pricing power and operational necessity. Networks have a duopoly over the rails. Processors provide technical infrastructure that merchants can’t easily build themselves. Issuers take fraud liability and fund rewards programs. Each layer justifies its cut by providing something merchants or consumers need.

Now agents come along and potentially disrupt every piece of this.

What changes when agents control transactions

Agents don’t need advertising. They don’t browse. They don’t compare. They execute.

When a user tells ChatGPT, “Buy me the best wireless headphones under $200,” the agent searches, evaluates, selects, and completes checkout in seconds. No Google Shopping ads. No Amazon-sponsored listings. No affiliate links. Just algorithmic selection based on parameters.

This threatens $459 billion in annual commerce monetization that depends on human discovery.

Retail media commands $140 billion in global revenue.

Google Shopping and search ads generate $238 billion.

Meta’s platform advertising adds $165 billion.

Affiliate marketing contributes $18.5 billion.

All predicated on humans browsing, discovering, and considering brands. Agents automate that away.

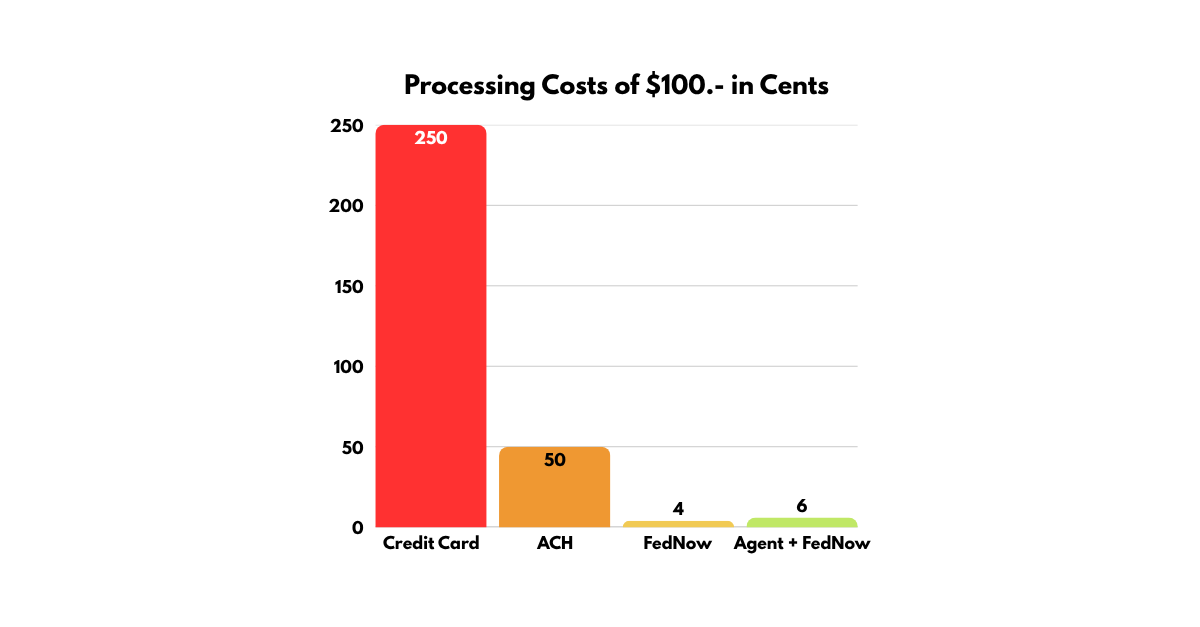

The interchange pool faces even more direct pressure. Agents optimize for cost and speed, not rewards points. FedNow charges $0.04 per transaction. Credit cards charge $2.50 on that same $100 purchase.

If agents shift transactions from cards to account-to-account instant payment rails, the revenue implications are massive. At 50% displacement, US card networks and issuers lose $56 billion annually. At 80% displacement, matching Brazil’s Pix trajectory, the loss hits $90 billion.

But here’s where it gets interesting for payment infrastructure providers.

The new value chain doesn’t eliminate fees. It adds a new layer.

AI platforms now sit between consumers and merchants, controlling discovery and recommendation. They want to get paid. But the foundational protocols connecting platforms to payment infrastructure deliberately charge nothing.

So where does margin actually live?

The new fee stack: six layers, different pricing power

Agent transactions currently cost merchants roughly 0.5-1% more than human transactions.

A $100 agent-initiated purchase costs around $3.60-4.10 versus $3.10 for traditional e-commerce. That extra 50-100 basis points goes to platform fees and agent-specific infrastructure. But the critical question: who captures what as this matures?

Let me break down the six-layer value chain.

Layer 1: Issuing banks. Still capture 1.5-3% interchange depending on card type. If the transaction runs on cards. But agents create pressure to shift to A2A rails where issuers earn nothing. The strategic move: diversify beyond interchange to account services, float, and data monetization.

Layer 2: Card networks. Charge 0.13-0.15% assessment fees on card transactions. Visa and Mastercard maintain this whether an agent or human initiates payment. Both launched agent-ready tokenization in April 2025, Visa’s Intelligent Commerce and Mastercard’s Agent Pay, with no disclosed premium fees. Yet. The strategic question: do networks add agent-specific surcharges once adoption scales, or compete on service value to defend standard rates?

Layer 3: Payment processors. Add 0.3-1% markup for their services. Adyen’s CFO said agentic integration requires “not real significant work,” signaling processors face commoditization pressure. Stripe’s differentiation comes from co-developing ACP with OpenAI, positioning as the path of least resistance. If ACP becomes the standard, Stripe benefits even when merchants use other processors. That’s strategic positioning, not transaction fee extraction.

Layer 4: Protocol providers. Charge nothing. Zero. Stripe offers Shared Payment Tokens with “as little as one line of code” integration for existing merchants at standard processing rates. Non-Stripe merchants can implement ACP with their existing processors at no protocol premium. Google’s AP2 operates identically. Free to adopt. Payment-agnostic. Monetization happens through participants’ existing services, not protocol tolls.

Why give away protocols?

Standard-setting power.

If your protocol wins, you influence the infrastructure layer. Stripe benefits from ACP adoption regardless of who processes payments. Google defends $238 billion in annual search advertising by ensuring agents route through AP2 infrastructure, where Google maintains relevance.

Layer 5: AI platforms. This is where the new margin lives. OpenAI charges a “small fee on completed purchases” through ChatGPT but won’t disclose the percentage. Industry analysis estimates 0.5-2% based on competitive benchmarks. Sam Altman suggested a 2% affiliate fee for purchases through ChatGPT, aligning with e-commerce affiliate norms of 5-15%. But nobody knows actual economics.

Google doesn’t disclose AP2 monetization. Likely treats it as strategic defense, protecting search relevance rather than direct transaction fees. PayPal positions itself as a platform-agnostic facilitator, charging standard merchant fees of 2.9% plus $0.30 across its partnerships with OpenAI, Google, and Perplexity. The economic model: enable all platforms, capture processing volume, avoid picking winners.

The precedent from search and marketplaces suggests platform take rates of 5-10% once these mature. Google Shopping captures 76.4% of retail search ad spend. Amazon charges sellers 8-15% referral fees. But early adoption pricing remains light. Build ecosystems first. Extract rent later.

Layer 6: Authentication and identity. Know Your Agent systems require new infrastructure. Cloudflare’s Web Bot Auth partnership with Visa and Mastercard positions it as the standard agent verification protocol. Pricing unknown. Likely bundled into network or processor fees initially. Long-term could become a separate fee layer if verification complexity requires it.

Here’s the math on what this means.

Today’s $100 human-initiated credit card purchase costs merchants $3.10. Tomorrow’s $100 agent-initiated transaction could cost $4.85 if platforms reach marketplace economics and networks add agent premiums.

That’s:

$2.70 in interchange with agent premium,

$0.15 in assessment,

$0.50 in processor fees, and

$1.50 in platform take rate.

A 57% increase in merchant cost.

The economics only work if agent-driven volume grows enough to offset higher per-transaction costs. Or if volume shifts to low-cost A2A rails, where the total fee stack compresses dramatically.

Payment rail economics: the $90 billion question

This is where the payments world gets disrupted.

Cards command 1.5-3% interchange. FedNow charges $0.04 flat. ACH runs $0.40-0.50. Real-time payment networks cost $0.01- $ 0.10. Agents optimize for cost and speed, not consumer rewards. The economic arbitrage becomes overwhelming.

Three scenarios quantify the impact.

At a 20% volume shift from cards to A2A rails, US card networks and issuers lose $22 billion annually. At 50%, losses hit $56 billion. At 80%, matching Brazil’s Pix adoption curve where instant payments overtook cards within four years, the revenue loss reaches $90 billion.

The precedent exists.

India’s UPI processes 640 million transactions daily, exceeding Visa’s global volume, with zero consumer fees. Brazil’s Pix reached 160 million users within four years, processing more than credit and debit cards combined. Both markets show instant payment systems achieving dominance in 3-5 years when conditions align: government backing, mandatory bank participation, zero consumer fees.

The US will take longer.

Fragmented banking. Strong card incumbency. Consumer attachment to rewards funded by $30 billion+ annual interchange. But FedNow launched in July 2023. The infrastructure exists. McKinsey projects US A2A payments exceeding $200 billion by 2027, up from near-zero in 2022.

Europe moves faster.

All payment service providers must receive instant payments by January 2025, send by October 2025. SEPA Instant Credit Transfers now account for 12% of volume but could reach 45% by 2027. The Netherlands already runs 64% of e-commerce via A2A.

Card networks execute three defensive strategies.

First, build A2A capabilities directly. Visa launched A2A bill-pay in the UK with fraud monitoring. Mastercard introduced Mastercard Move for real-time B2B settlement.

Second, diversify revenue beyond interchange. Value-added services such as fraud detection, analytics, and tokenization grew by 16-20% annually across both networks.

Third, reposition as “general networks” rather than card-specific processors.

The strategic question for networks: can you prove enough value through fraud prevention, dispute resolution, and authentication to justify premium pricing when A2A rails cost 98% less?

Where margin concentrates: infrastructure versus distribution

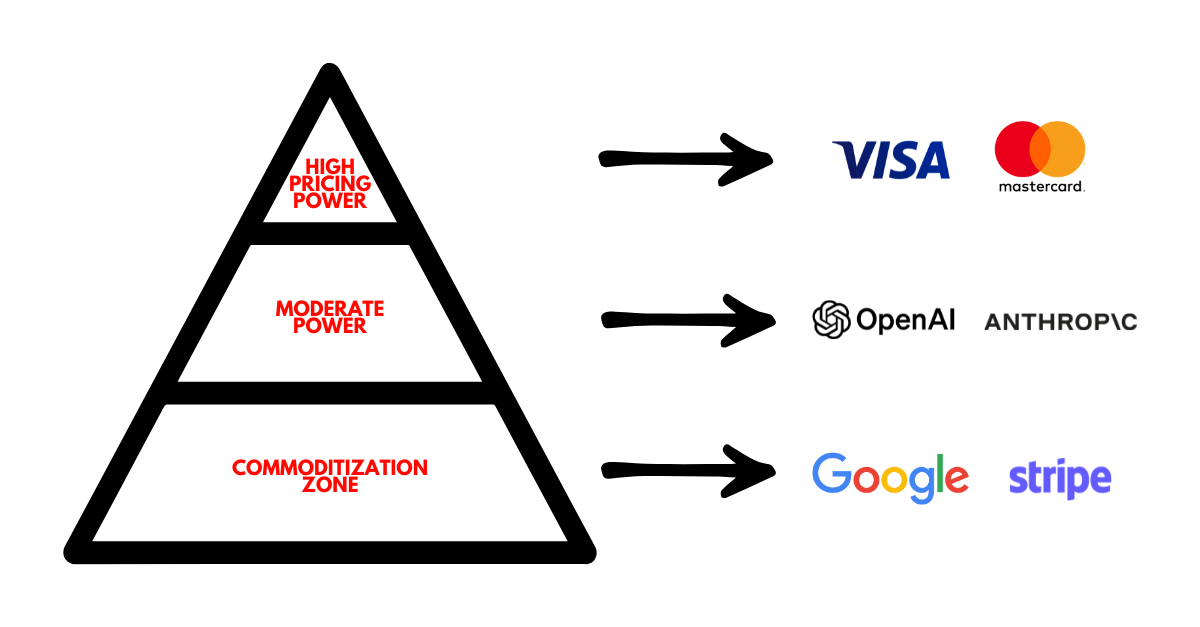

Here’s the fundamental economic principle. Pricing power is concentrated in two areas: infrastructure control and distribution control. Everything else faces commoditization pressure.

Infrastructure control means owning the rails. Visa and Mastercard’s duopoly commands 90% of global card volume despite decades of regulatory pressure. Massive fixed costs. Low marginal costs. Regulatory barriers to entry. Data network effects from fraud detection. That’s natural monopoly territory. Stripe leads with 20.8-29% market share in payments processing, co-developing protocols with OpenAI and embedding integrations across Shopify, Etsy, and thousands of merchants. The “path of least resistance” for agent payments runs through Stripe even as AP2 offers alternatives.

Distribution control means owning consumer attention. OpenAI’s ChatGPT commands 800 million weekly users. Google’s Gemini reaches 1.5 billion monthly users via AI Overviews and Search integration. These platforms control the suggestion algorithms, the core gatekeeping function that determines merchant visibility. This parallels Google’s search dominance or Amazon’s product placement, both of which command premium fees. The precedent suggests 2-3 dominant platforms capturing 70-80% of general-purpose agent interactions.

Everything between infrastructure and distribution is subject to commoditization. Payment processors whose integrations require “not real significant work” have minimal pricing leverage. Protocol providers give away their technology to win standard-setting battles. Merchants remain price-takers, absorbing fee increases as they always have.

The predicted market structure resembles mobile platforms. Concentration at OS and distribution with iOS and Android duopoly. Concentration in infrastructure with AWS, Azure, GCP oligopoly, and Stripe dominance in payments. Fragmentation in applications with millions of apps in a power law distribution.

Applied to agentic commerce: OpenAI and Google capture 60-80% of general-purpose agent interactions. Stripe plus adapted card networks dominate payment processing. Hundreds of vertical-specific agents serve long-tail needs. Value capture splits roughly 30-40% infrastructure layer, 30-40% distribution layer, 20-40% application layer distributed across many players.

Infrastructure costs: declining but front-loaded

Large payment processors face initial buildouts of $28-55 million for agent infrastructure.

API development runs $5-10M.

Agent authentication systems cost $8-15M.

Fraud detection evolution requires $10-20M.

Compliance and legal add $3-5M.

Testing and integration consume $2-5M.

Annual operating costs add $13-22M.

Infrastructure maintenance at $5-8M.

Compliance monitoring at $3-5M.

Fraud operations at $4-7M.

Protocol participation at $1-2M.

But marginal costs decline toward zero.

LLM inference costs dropped 1,000x in two years from 2021 to 2023. Current pricing ranges from $0.06 per million tokens for Llama 3.2 to $0.50-5 for production implementations. At a 10,000-word-per-hour speech rate, continuous agent operation costs under $1. Making inference costs negligible relative to transaction values.

This cost structure enables micro-transactions economically impossible under card interchange.

A $5 purchase paying 2.9% plus $0.30 costs merchants $0.445, or 8.9% of the transaction value. The same purchase via FedNow costs $0.04 with agent inference adding perhaps $0.02, totaling $0.06 or 1.2%. An 87% cost reduction.

The strategic implication: scale matters.

Fixed infrastructure costs of $30-50M favor large processors who amortize across volume. Small processors struggle. A 0.01% premium on $100 billion annual volume generates $10 million, achieving break-even within 2-3 years. But you need the volume first.

What payment infrastructure providers should do

The window to establish a competitive position is closing.

Action timelines: 2025-2026 for strategic positioning.

2027-2028 for mainstream adoption.

2029-2030 for mature market structure.

Companies not positioned by 2026 face reduced optionality.

For payment networks: The strategic choice is to own the infrastructure or become commoditized.

Visa and Mastercard implement defensive tokenization as they build A2A capabilities. Diversifying revenue into value-added services, growing 16-20% annually. Positioning as “general networks” rather than card-specific. This maintains relevance by shifting volume off cards while protecting existing interchange. But success requires continued innovation, justifying premium pricing over commoditized A2A rails.

For payment processors: Differentiation comes from protocol positioning and ecosystem integration, not transaction processing.

Stripe’s advantage: co-developing ACP with OpenAI. One-line integration for existing merchants. If ACP becomes standard, Stripe benefits from every ChatGPT, Perplexity, and third-party agent regardless of a direct processing relationship. That’s strategic positioning. For other processors: integrate with dominant protocols now, build value-added services beyond commodity processing, or accept commoditization.

For AI platforms: The choice is to monetize aggressively or build an ecosystem first.

OpenAI prioritizes trust and adoption over immediate revenue extraction. But Sam Altman’s 2% affiliate-fee suggestion signals the likely path: performance-based commissions aligned with e-commerce norms. The strategic question: how much can platforms charge before merchant resistance or consumer trust erosion limits growth?

For infrastructure providers generally: Invest in agent-specific capabilities now.

API integration for agent workflows. Authentication and identity systems for Know Your Agent. Fraud detection adapted to agent behavior patterns. Mandate management infrastructure. These investments pay off if you capture the protocol layer or become essential infrastructure that platforms and processors must use.

The companies that define fee structures, establish protocols, and build distribution in 2025-2026 will capture disproportionate value. Those that wait risk commoditization, dependency, or irrelevance.

Thank You for Reading. Please like, Comment, Share, or Post on Your Social media. I appreciate all the feedback I can get.

P.S. If you’re interested in collaborating with me, whether through speaking, advisory services, or consulting, please don’t hesitate to email or DM me.

Or if you appreciate my work, feel free to buy me a coffee!

Wow, the part about the gap between free protocols and opaque platform fees really stood out to me. You’ve perfectly articulated the core tension here. From a public policy angle, this transparency deficit by platforms like OpenAI is a fascinating challenge. It makes assessing market fairness and potential regulitory needs quite tricky, especially for us trying to ensure an equitable digital economy for everyone.

Love this breakdown! There is an underlying assumption that agents will always optimize for cost and speed. That feels right for the next 3–5 years while platforms build trust and keep agent behavior predictable.

But who ultimately controls the agent’s incentive model if factors expand to rewards, loyalty, or merchant incentives. The economics likely shift upstream from rails to the agent layer.

Curious how you see that playing out. Do processors, merchants, or the platforms themselves get to define what the agent optimizes for?