Agentic Adoption

The £29 Billion Gap Between What’s Being Built and What Consumers Want

The industry spent 2025 building autonomous AI shoppers.

Google released Agent Payments Protocol with 60-plus partners. Mastercard introduced Agent Pay. Visa rolled out Intelligent Commerce. All designed to one day allow AI agents to browse, compare, select, and buy without human intervention.

Then, Worldpay surveyed 8,000 consumers across seven countries to see if anyone actually wanted this.

The data says no. Well, not exactly, no. More like “not yet” and “not like that.”

Here’s the disconnect.

The approval step isn’t something to eliminate through better AI. It’s the feature that enables adoption.

The £29 Billion Misunderstanding

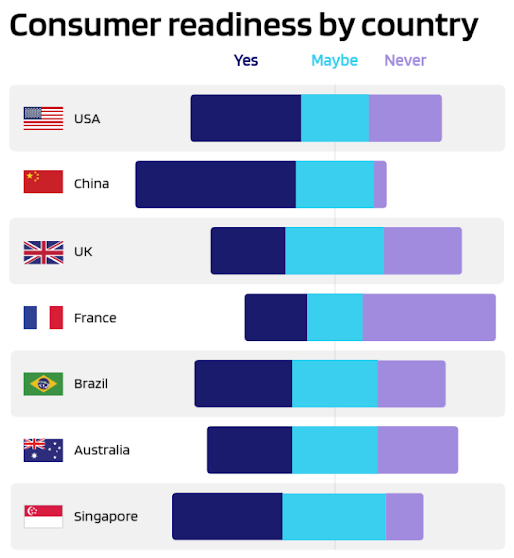

By 2030, consumers expect AI agents to handle 7% of their online purchases. In the UK alone, that’s £29 billion flowing through bots.

But here’s what the protocols missed.

Globally, 40% of consumers say they’re ready to let AI help them shop. Browse products, compare prices, and find deals. Among 18-34-year-olds, this rises to 45% in the UK.

Ask those same people whether they’d allow AI to complete purchases without first checking, and the number drops to 6%.

Forty percent want help. Six percent want autonomy. That 34-point gap is the entire market, and almost everyone in payments built for the wrong side of it.

[“Consumer readiness by country”, Worldpay Agentic Commerce Report, page 3]

What Shoppers Actually Want

The pattern holds across nearly every market surveyed by Worldpay.

In the US, 40% would let AI browse on their behalf. Only 9% want it to buy automatically. UK shoppers exhibit similar caution: 31% for browsing and 6% for autonomous checkout. France is even more sceptical at just 3%.

The age splits tell you where this eventually goes, but they don’t change the near-term reality. Even among 18-34-year-olds, fewer than 15% prefer fully autonomous purchasing. They want assistance with approval, not automation without oversight.

[“How much control would you want over purchases made by an AI agent?” , Worldpay Agentic Commerce Report, page 12 (UK data).]

The Three Trust Barriers

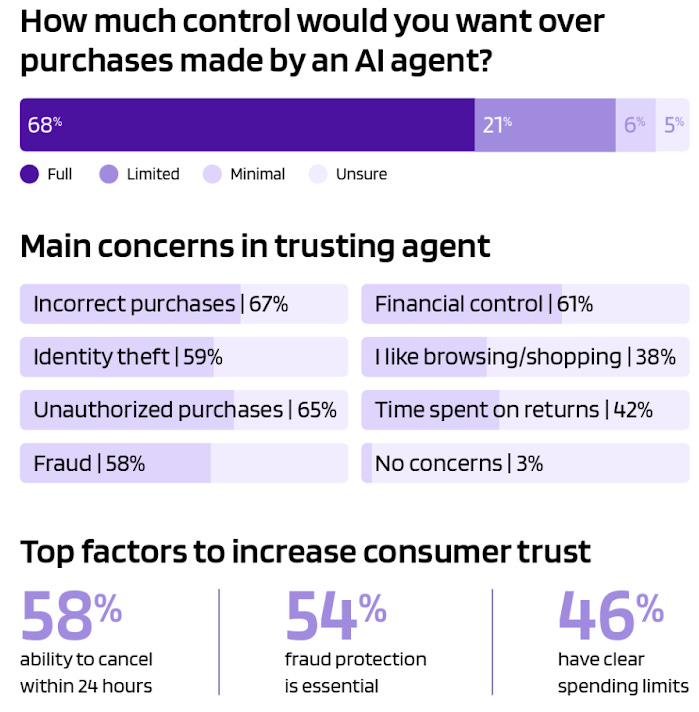

Worldpay asked what would need to exist before consumers trusted AI shopping agents. Three barriers dominate.

1. Incorrect Purchase Fear

Sixty-seven percent worry that an agent will buy the wrong thing. Think about how often autocomplete predicts exactly what you meant to say. Now imagine that autocomplete can spend your money.

This explains why 60% of respondents demand the right to review transactions before completion. They want to see what the agent selected, verify the price, confirm details, and then approve. The approval step isn’t a nice-to-have. A guardrail that all protocols have already put in place.

Another 58% won’t trust an agent without 24-hour cancellation rights. Even if they approved the purchase, they want an escape hatch.

2. Financial Control

Fraud protection ranks as the number one trust requirement globally. Fifty-four percent say they need confidence that agents can’t be manipulated before they’ll adopt.

This isn’t about normal e-commerce fraud where someone steals your card. This concerns what happens when an AI agent is tricked into buying items you never authorized. Think of it like a professional personal shopper who shows up with a $500 watch because someone at the store convinced them you’d love it.

Here’s the technical problem. Legacy fraud systems watch for suspicious human behavior. Multiple purchases in quick succession, impossible geographic travel, abnormal session patterns. An AI agent violates every rule during normal operation. It can verify 20 merchants in 60 seconds and transition from discovery to checkout in under 1 second. To traditional systems, this looks identical to fraud.

Forty-six percent want explicit spending limits on agent activity. Not account limits. Agent limits. They want to tell the AI: you can spend up to £200 per month on groceries, £50 on household supplies, and nothing on electronics without asking first.

These limits work like a financial power of attorney. Specific authority with defined boundaries. The agent can act within those boundaries, but it can’t exceed them, no matter how good the deal looks.

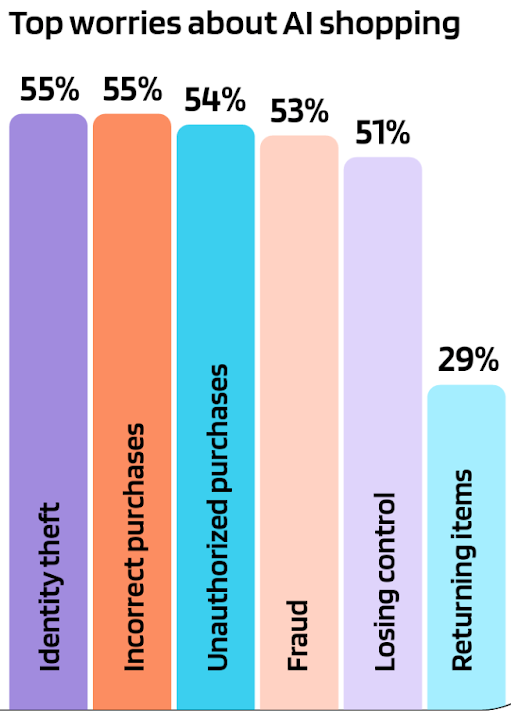

[“Top worries about AI shopping”, Worldpay Agentic Commerce Report, page 4.]

3. Human Support Access

Forty-four percent won’t trust an agent unless they can reach a real person when things go wrong.

Pure-AI shopping experiences face an economic contradiction. You can’t eliminate customer support costs if half your potential users demand human escalation paths as a precondition for adoption.

People want AI to do the boring work. They want humans available when the work stops being boring and starts being important, expensive, or wrong. For agentic commerce, that includes most purchases over £100 and anything involving returns or disputes. The transactions where margins actually exist.

Why One Agent Can’t Rule Them All

These three barriers don’t just block adoption universally. They manifest completely differently in each market, requiring fundamentally different approaches.

The Tale of Two Extremes

China shows what’s possible when infrastructure precedes agents. Seventy-two percent cite speed and convenience as the primary draw. 35% would accept fully autonomous purchasing today, rising to nearly 80% among younger consumers.

Why the difference?

Mobile payment infrastructure in China already operates at speeds that make agents feel like an incremental improvement rather than a fundamental shift. When you’re used to buying through WeChat by tapping twice, having an AI do it isn’t a big leap. The trust exists because the infrastructure proved itself trustworthy first.

The UK represents both a mainstream opportunity and a challenge. Thirty-one percent are willing to let AI browse. Only 6% want autonomous buying.

The top trust requirements skew heavily toward security. Fraud protection (54%), 24-hour cancellation (50%), and purchase review (49%). British consumers want multiple safety mechanisms before they’ll hand over purchasing authority to an algorithm.

Value matters too. Sixty-one percent cite cost savings as a reason to adopt. But security concerns outweigh cost benefits. An agent that saves £10 but creates uncertainty about unauthorized charges isn’t worth the savings.

This pattern defines the mainstream market. The companies building for this 31% will capture the £29 billion. Those building for eventual Chinese-style adoption will wait years for a future that may never materialize in Western markets.

The Orchestration Gap That Has Been Overlooked

The protocols solved message formats. They defined how agents communicate with payment systems, how mandates get created, and how credentials get tokenized.

What they didn’t solve: the orchestration layer that makes consumers comfortable with what those agents do.

Look at what the market actually requires for the 31% who want collaborative shopping.

Real-time approval workflows that don’t feel like friction. When an agent finds the product you asked for, you need to review and approve it in under five seconds. Any longer and the efficiency benefit disappears.

Fraud protection operating at agent speed. Traditional systems take 300-500 milliseconds to score a transaction. Agents complete entire purchase flows in under one second. The fraud analysis must occur faster than the shopping process.

Identity verification that doesn’t break agent workflows. SMS codes can’t reach agents. Biometric authentication requires biological traits that agents don’t possess. The verification has to happen at the protocol level, not the checkout level.

Programmatic cancellation systems. Not manual request forms. Cancellation that agents can execute on user instructions without human intervention.

Human support escalation is integrated with agent activity logs, with staff trained to address agent-specific issues and to recognize when an agent transaction requires human review.

Dispute and chargeback handling for agent-initiated transactions. The existing system assumes a human clicked buy and now claims they didn’t. What happens when the human authorized an agent, the agent executed within its mandate, but the human disputes the charge anyway?

Why Merchants Can’t Build This Themselves

Here’s what the technical stack actually looks like.

Visa or Mastercard rails for payment processing. Google’s AP2 for agent protocols. Multiple fraud-detection vendors, because no single provider catches everything. Identity verification services for agent registration. Approval workflow systems for real-time user confirmation. Dispute handling infrastructure for agent-specific scenarios. Compliance frameworks that vary by market. Different data localization requirements, different authentication standards, different consumer protection rules.

Then configure all of it differently for each market. UK merchants need fraud protection first, cost optimization second. US merchants need cost optimization first; fraud protection is a table-stakes requirement. Chinese merchants need speed above everything.

Most merchants can’t wire this together themselves. Even large retailers struggle to integrate multiple payment providers, fraud vendors, and compliance frameworks into a single coherent system. When the complexity of agent-specific requirements (sub-second fraud detection, programmatic cancellation, mandate validation) is added, it becomes impossible without significant infrastructure investment.

This is precisely the orchestration gap that platforms like Worldpay are addressing. By connecting protocol layers like AP2 with payment rails (Visa, Mastercard), fraud detection, identity verification, and compliance frameworks into a unified infrastructure, they enable merchants to support agentic commerce without rebuilding their entire payment stack. Worldpay does the heavy lifting of connecting to the various protocols and has the tools and resources to keep these transactions safe and secure.

The value in agentic commerce doesn’t come from having the smartest agent or the fastest protocol. It stems from having infrastructure that connects all these pieces together, thereby increasing the 31% who trust the agent’s recommendations.

Because that 31% is where the £29 billion lives.

What Actually Gets Built

The industry spent 2025 obsessing over autonomous agents. Build the AI smart enough, make it fast enough, get the protocols right, and consumers will hand over purchase authority.

Worldpay’s data reveals a different path.

Consumers will hand over browsing and comparison first. They’ll approve purchases manually for a while. Then, gradually, as they build confidence that the agent understands their preferences and doesn’t make expensive mistakes, they’ll expand the mandate.

This adoption curve changes what needs to be built.

You don’t need agents that operate completely independently. You need agents that collaborate smoothly. The approval step isn’t something to eliminate through better AI. It’s the feature that makes people comfortable expanding what they let the agent do.

The companies that understand this will build differently. Not for 2030 autonomy, but for 2027 adoption. The approval workflow becomes the core product, not a stopgap until the AI improves.

The trust infrastructure becomes the differentiator, not the agent’s recommendation algorithm.

And the orchestration layer that wires together fraud protection, identity verification, approval flows, and dispute handling across multiple providers becomes more valuable than the protocol layer everyone spent 2025 fighting over.

The £29 billion opportunity is real. But it materializes only if the infrastructure exists to support it. The companies that build for what consumers want today will capture the market before those that build for what they think consumers will want eventually.

Want The Complete Analysis?

The full Worldpay Agentic Commerce Report includes detailed country-by-country breakdowns across all seven markets, complete trust-requirement data by demographic, generational adoption patterns and timelines, and market-readiness analysis showing which regions will adopt first and why.

Great article, Dwayne. I’m not convinced surveying customers here is that useful or objective. It's a bit like asking people what they thought about the internet before it existed.. when nobody wanted it. Or more recently, pre ChatGPT, whether they’d be comfortable handing over so much data to a chatbot.

These kinds of changes just aren’t something the mass market can really reason about until they’ve experienced them. What’s more interesting to watch is how people actually behave once they use those tools, the adoption patterns, the new behavioural habits, and then use those signals to predict the trajectory.

It’s pretty clear to me we’re heading towards handing off as much work as possible to agents and as you rightly said, gradually letting them operate on their own within clear guardrails and boundaries. This could move a lot faster than we expect. Just look at how fast clawdbot took over the tech world over the last few days, how quickly people plugged in their data, and how easily they gave it permission to handle payments, order lunch, groceries, bookings, etc. Just because it was super useful (and models are very good at persuading you they can get the job done).

One other thing worth thinking about: once agents start making payments on our behalf, they’ll also start optimising how those payments happen and nudging adoption of certain technologies or networks over others. That kind of influence can massively accelerate change, similar to what we saw in other areas like how Ai tools pushed TypeScript to take over front-end engineering in no time (overtook Python & Javascript on Github in less than 1 yr).

"The companies building for this 31% will capture the £29 billion." This is a glass half full characterization. The other is that the £29 billion could be reduced by 2/3 if 31% is closer to 10%.